By Erick Muller, Director of Product and Investment Strategy, Muzininch & Co

Since mid-2016, we believe diversified investors have been exposed to ‘momentum’ trades – betting on the strength of the global economic cycle and designing portfolios to benefit accordingly. The result was a large overweight in equity markets, often financed via fixed income.

However, the disruptive tail risks that emerged last year, such as US trade wars, monetary policy tightening, Brexit and the Italian budgetary issues in Europe and crises in Turkey and Argentina in emerging markets, weighed on these positions.

We believe the significant sell-off towards the end of last year changed the return expectations for 2019, and we could see a further shift away from momentum trades towards value/income trades, given more attractive valuations.

With better valuations and softer global growth, but no recession likely, we believe the case for balanced portfolios to reconsider their credit allocation appears compelling.

Fundamentals – the Focus on Investment Grade BBB

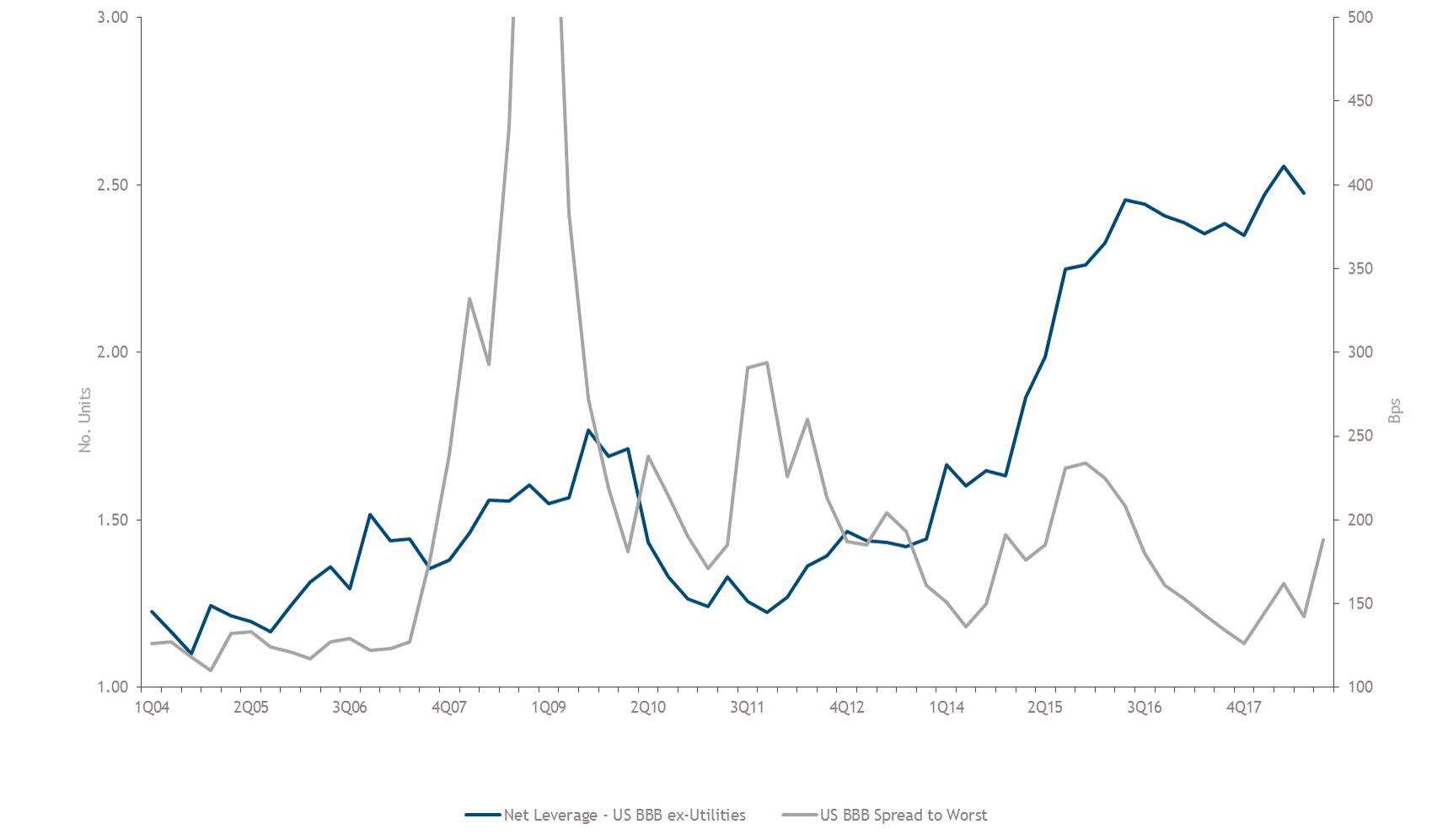

The fundamental backdrop evolved notably in 2018, particularly in the US. Overall, US non-financial debt increased (Fig. 1), mainly due to rising leverage ratios in investment grade credit (Fig. 2).

Fig. 1 – US Non-Financial Corporate Debt and Assets as a % of GDP

Fig. 2 – Rising Leverage in US Investment Grade

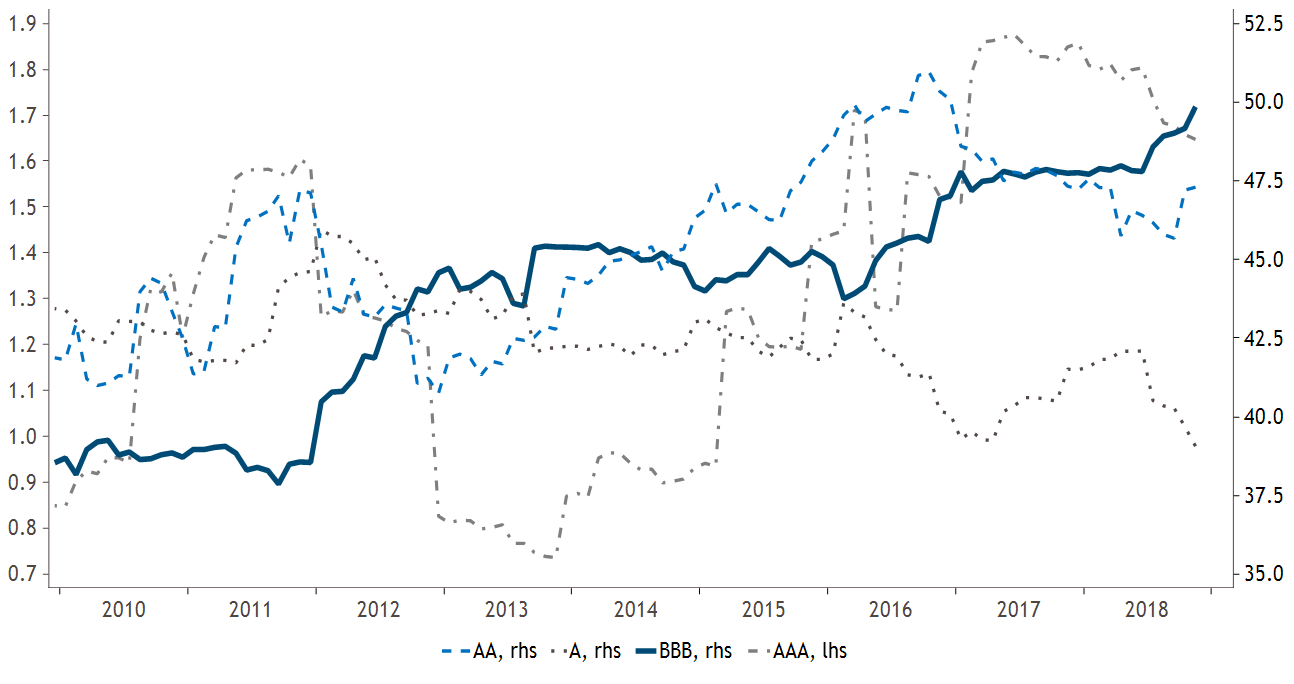

The current concerns are less about an unwarranted rise in the default rate in the high yield market, and more about investment grade, where the BBB rated segment continues to grow (Fig. 3).

Fig. 3 – Evolution of Ratings Segment as % of Total Market Cap

The fear of market participants comes from the current size of the BBB non-financials segment ($2.4trn) that could suffer from further negative credit migration, compared with the size of the high yield market ($1.2trn), and more specifically the BB segment ($570bn).[1]

We would moderate these concerns however as the BBB- non-financials segment represents “only” US$736bn, of which Goldman Sachs estimates $164bn are under negative watch, and of which US$10bn have a more severe downgrade watch status.[2]

Moreover, for such a cataclysm to materialize, corporates would need to ignore the current market message and continue to increase leverage, or for a severe revision to economic growth to hit current forecasts. Although this remains a risk, it does not form our base-case scenario.

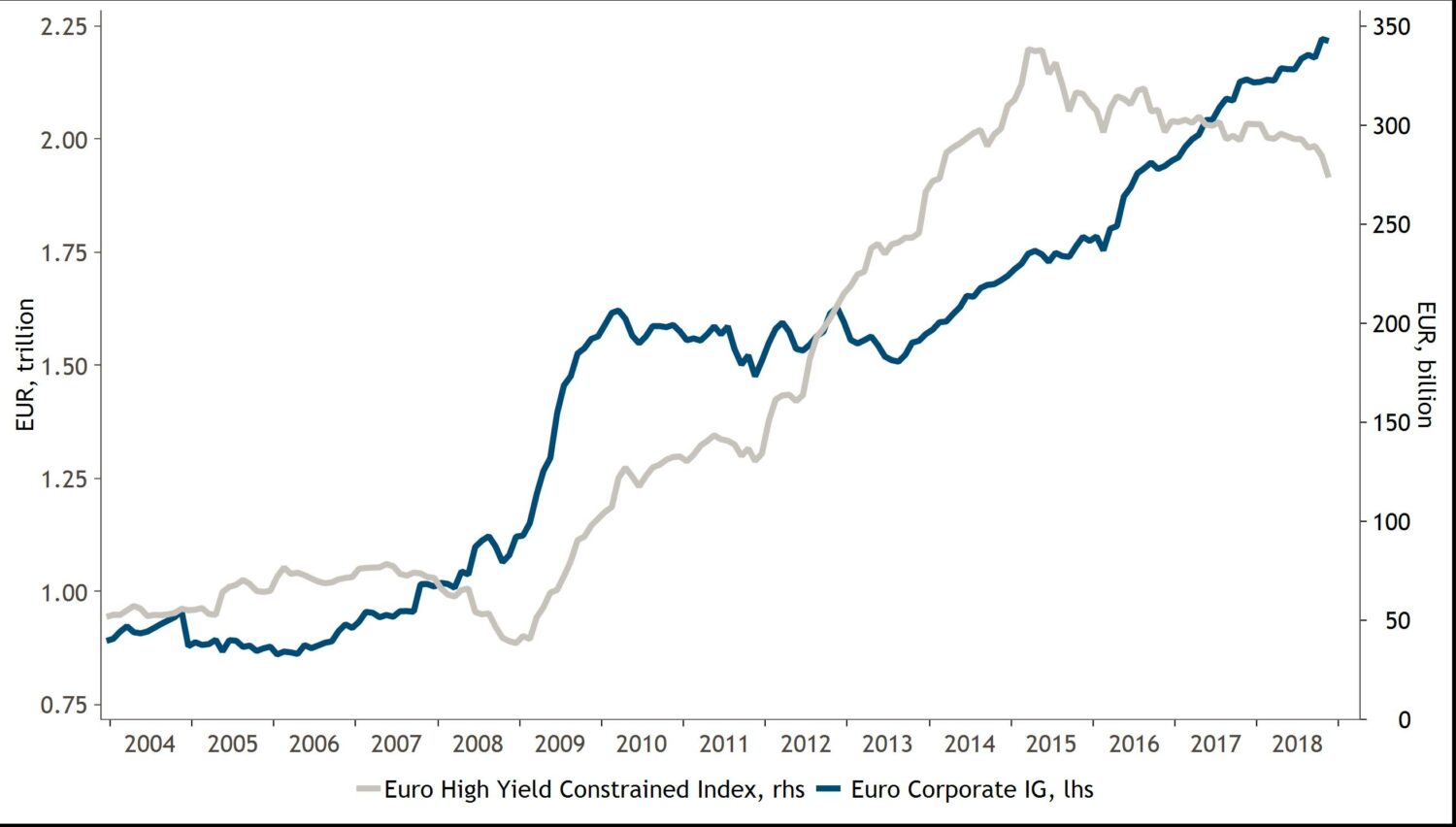

The European investment grade market is not immune from investor concerns. The growth of this segment has been rapid, boosted by the ECB’s quantitative easing programmes and heavy issuance policies from corporates benefiting from private investors shifting from government bonds into investment grade rated corporate bonds. Here, the contrast between the growth of the European investment grade market and the shrinkage of the European high yield market is notable (Fig. 4).

Fig. 4 – Market Cap Evolution for EUR Credit IG and HY

However, while there are some uncertainties around the European political situation, we believe there are several factors that could prove positive for European credit. Private consumption in the euro area appears solid, with improving employment, while private investment spending remains resilient. Moreover, fiscal policies should be relaxed somewhat in a counter-cyclical action.

The fundamental outlook for emerging economies is expected to contrast with advanced economies and improve in 2019; we could see Brazil and Mexico benefiting from lower political risk premium and more market-friendly policies.

While Asia may face the risk of a further slowdown in the Chinese economy, our central scenario is that the very extensive growth stimulus programmes put in place by the Chinese leadership may ultimately offset the negative impact of the trade tariffs imposed on Chinese exports to the US.

Valuations – Wider Spreads but is it Enough?

Tight valuations were often quoted as the main reason for underweighting credit in balanced portfolios. However, credit sold off during the second half of last year and we believe the resultant attractive valuations could compete better relative to other asset classes in 2019.

Meanwhile, cross currency hedging costs between the US and Europe will likely remain on an upward trajectory if the Fed continues its rates normalisation policy.

The hedging cost benefit for US dollar based investors comes with a hidden gift – low volatility. In a less predictable macro environment, we believe such a gift is worth a considerable amount for US dollar based investors. However, these hedging costs are also an obstacle for euro or Japanese yen based investors to invest in US dollar-denominated assets, a hurdle that may keep European savings in domestic markets.

The significant repricing of emerging market credit started in May 2018. Heavy supply, combined with trade war concerns, hit emerging market debt at cycle tights throughout last summer.

In our view, the correction towards the end of last year preserved the asset class in relative terms to US or European credit. Nevertheless, spreads continued to widen to levels that many would consider attractive. Meanwhile emerging market corporates may well appear as one of the main beneficiaries of the search for yield in the context of stable US short rates.

With the direction of US growth less predictable this year than last, there is no longer any consensus on the direction of the dollar, something that we expect could also play in favour of emerging market financial assets.

However, for new valuations to be attractive enough to investors, we believe spreads have to compensate them for two factors of uncertainty – the economic cycle and higher volatility – and to provide a premium versus other asset classes. However, the rally in January and early February has removed credit markets from the status of cheap to fairer value.

Technicals

Technicals (supply and demand dynamics) have been very different from one region to another.

The US high yield market was notoriously undersupplied in 2018. The investment grade market was well supplied in the first half of last year, but was less so during the more volatile second half.[3] At the same time, the loan market funded alternative for corporates in the high yield space with a net issuance of US$434bn over the year. [4]

The supply profile of the European corporate credit markets has been different. Corporates have benefited from the ECB’s corporate sector purchase programme (CSPP) by issuing CSPP eligible bonds. This has resulted in a significant growth of the European investment grade market. Most of this growth has come from BBB rated companies, a similar pattern to the US. In our view, the rise of US yields has not however encouraged other investment grade issuers to issue longer-dated paper as they have in previous years.

What made a significant difference in 2018 was on the demand side where outflows hit all credit markets across the US and Europe.

If these technicals have been a clear negative all year long, it also means that the ‘tourist’ money – aimed at opportunistically capturing yields during heavy cash inflows linked to central bank quantitative easing programmes – have progressively shifted away from these investments and moved back to equities or core fixed income.

We noticed that institutional investors, remarkably absent during the various hiccups in 2018, appeared to be contemplating valuations with more appetite, in particular vis-a-vis the equity market towards the end of last year. We believe the extreme positioning seen in 2018 in favour of equities is unlikely to be replicated this year.

The Return of Value

In our view, the mix of more attractive valuations in credit markets, combined with a ‘Goldilocks’ scenario (i.e. not too hot or too cold) for the global economy in 2019 and stable US short rates could reinvigorate institutional and retail demand for credit, particularly in high yield.

However, in our opinion, for such interest to manifest itself into significant inflows, the current macroeconomic uncertainties have to dissipate, namely trade wars and the stabilization of the Chinese economy.

High margins and low volatility are arguments that play in favour of loans for euro-denominated portfolios. Nevertheless, deteriorating fundamentals require us to be very discerning in issuer selection to enable us to aim to deliver positive returns.

We were reasonably comfortable with fundamentals and default rates in 2018, although found tight valuations unattractive. In our view, 2019 is likely to be a sharp contrast. Fundamentals will have to reflect lower macroeconomic prospects, their impact on profits and average leverage ratios and higher political risks. However, we believe Valuations now appear difficult to ignore and reinforce the prospects of achieving interesting positive absolute returns, in particular within higher-yielding credits.

Technicals should turn more positive but we believe some macroeconomic uncertainties have to be removed during the first quarter for this to happen.

In our view, this year may well see the return of value trades for global credit markets.

Fig 1 Source: Federal Reserve, as of 30 June 2018

Fig 2 Source: Macrobond, JPMorgan, as at Q3 2018. ICE BAML Index C0A1, C0A2, C0A3 indices US AAA-AA-A-BBB rated corporate, as at December 14, 2018.

Fig 3 Source: ICE BofAML US Corporate Index (C0A0), ICE BofAML AAA US Corporate Index (C0A1), ICE BofAML AA US Corporate Index (C0A2), ICE BofAML Single-A US Corporate Index (C0A3), ICE BofAML BBB US Corporate Index (C0A4), as of 30 November 2018

Fig 4 Source: ICE BofA ML Euro Corporate Index (ER00), ICE BofA ML Euro High Yield Constrained Index (HEC0), as of 30 November 2018.

[1] ICE BofA ML BBB US Corporate Index (C0A4), ICE BofA ML BB US High Yield Constrained Index (HUC1) as of 30 November 2018

[2] Goldman Sachs – The Credit Trader, Oct 25, 2018

[3] ICE BofA ML US Cash Pay High Yield Index (J0A0), ICE BofA ML US Corporate Index (C0A0), as of 30 November 2018

[4] Deutsche Bank Global Credit ChartBook, S&P LCD US Loans Index, as of 30 November 2018