By Anna Lundén, CFA, Managing Director and Equity Portfolio Manager, Wellington Management

While the structural advantages of European small-cap companies are well documented, this asset class is sometimes seen as a difficult proposition for investors with a moderate risk budget or ESG requirements.

Yes, European small caps have exhibited better earnings growth, stronger balance sheets and higher shareholder returns on average than their large-cap peers (on an absolute and a volatility-adjusted basis). But with a higher overall beta and lower levels of corporate disclosure than large caps, this under-researched universe is accused of having high volatility, poor defensive qualities and little publicly available ESG data.

Wellington Management’s Pan European Small Cap Equity strategy, which has ESG considerations as part of its investment process, has not only outperformed the index1 in downturns as well as up markets; our alpha generation has actually been stronger in down markets.

How do we do it?

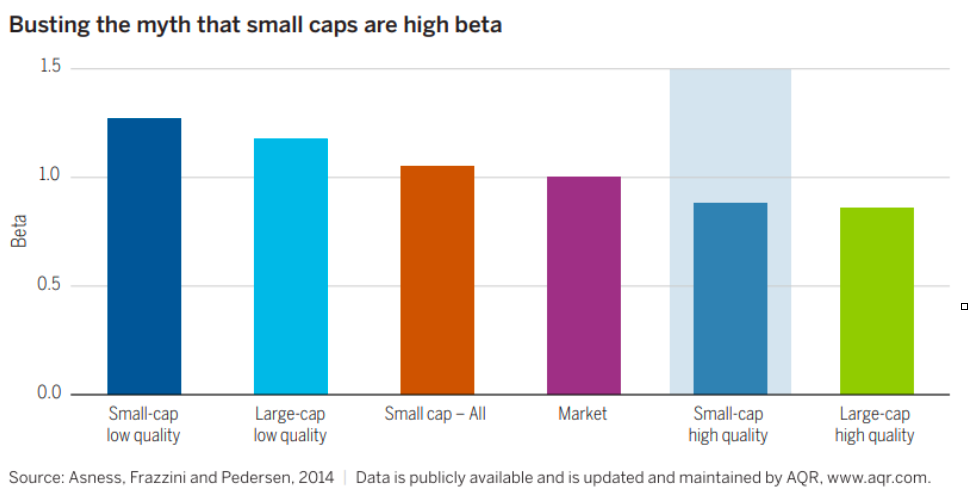

A large part of the explanation is that our investment process focuses on identifying high-quality companies with structural growth drivers. We’ve found that when companies that do not meet specific quality criteria are filtered out of the small-cap market, the beta of the high-quality segment that remains (defined as an average of profitability, growth, safety and payout) is lower than that of the overall market (see chart). We believe by stripping out these value traps from the small-cap universe, it is possible to harness the potential of this opportunity set without having to take on substantial market risk. In other words, our focus on quality reduces volatility.

We think that investing in innovative companies with structural growth drivers provides the basis for enhanced risk-adjusted returns in the long term. From a sustainability perspective, these twin focuses on growth and quality also help us to avoid many of the companies with the weakest ESG scores.

Lower levels of ESG information among small caps are still a reality — but one that we view as a market inefficiency and an opportunity for us to add value as an active manager. That’s because for us, ESG considerations are a crucial input to successful long-term investing. Failure to incorporate ESG principles can constitute a threat to the viability of a business, while positive action can support its growth. As a result, we actively want to align ourselves with companies that are ESG conscious. This means we need to know our investee companies inside out, which involves proactive engagement with company management and boards to understand a company’s approach, business model and market. How does the company visualise its risks and opportunities? What is their process for establishing the “materiality” of ESG concerns? This approach requires bespoke site visits to observe the production process, engagement with employees and company culture — and we are fortunate to be able to leverage Wellington’s scale and depth of research to benefit from superior company access.

Investing in small caps is research-intensive. But we believe the wealth of resources at Wellington Management allows us to call on multiple research perspectives, for example from our ESG research analysts, Fixed Income Credit Research Team and global industry analysts. Generating actionable and profitable insights from a sea of information also requires an experienced portfolio management team with specialist small-cap expertise.

When is the best time in the cycle to invest in European small caps?

In our view, another obstacle for smaller companies has been a perception of cyclicality — that they make gains in periods of economic expansion, but give them back in the later stages of the economic cycle.

We have found this is true for the universe as a whole, but that a focus on quality changes the picture considerably. While small caps overall deliver strong outperformance versus their large-cap peers in the recovery and expansion periods, and underperformance in late-stage and bust periods, the high-quality segment of the small-cap universe does not give its outperformance back in the late and bust stages. Instead, it matches large caps in the late stage and marginally outperforms in the bust stage.

As the Continent emerges from a steep recession, there is much uncertainty ahead. But we believe European small caps can and should be a long-term strategic allocation for investors and, with an emphasis on the higher-quality, lower-beta portion of the market, can continue seeking to deliver alpha throughout the economic cycle.

Sources:

1 Wellington Pan European Small Cap Equity Fund EUR S Acc vs MSCI Europe Small Cap Net (EUR) since inception (29 September 2017).

{kind=link}