By Hamlin Lovell, NordicInvestor

Many pension funds and asset managers are keen to emphasise engagement and less keen to discuss exclusion, but PenSam has one of the longest exclusion lists NordicInvestor has seen: 329 companies and 33 countries. NordicInvestor interviewed Mikael Bek, Head of ESG, to highlight some distinguishing features of PenSam’s exclusion and other ESG policies, which are part of its Responsible Investment and Active Ownership policy. PenSam manages approximately EUR 21billion of pension savings for both public and private sector employees in elderly care, cleaning, technical service and pedagogical care.

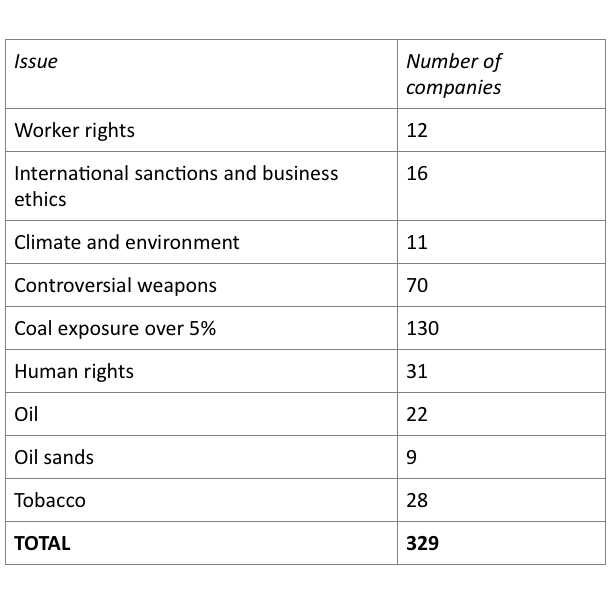

Six of PenSam’s exclusion categories are based on companies’ production or area of activity: climate and environment; controversial weapons (including nuclear bombs and cluster munitions); coal exposure over 5% (including both metallurgical/coking coal, and thermal coal); oil; oil sands; and tobacco. “The industry exclusions started with controversial weapons, then added coal in 2016 – initially with a threshold of 30% of company revenues, which has recently been cut to 5%. Tobacco was added in 2017, and oil in 2019″, says Bek and continuous;

We are quite aggressive on reducing exposure to fossil fuels. This is not only ESG but also good investment and risk policy because the sector will be under tremendous pressure over our 30 year time horizon….”

Corporate Conduct or Behaviour

Three of the exclusion categories are based on behaviour or conduct rather than activities: worker rights issues; human rights issues, or international sanctions and business ethics, based partly on the UN Global Compact. In theory, a company running wind farms or solar power could be excluded, if it was using child labour or slave labour, or perhaps involved in certain types of tax avoidance or evasion schemes.

Sustainalytics is retained to screen companies for both activity and behaviour.

As of October 2020, the PenSam exclusion list runs to a total of 329 companies.

This is roughly double than the Norges Bank Investment Bank (NBIM) list of 167 companies, and far more than the Swedish Government AP funds, which only excluded 29 companies as of their June 2019 exclusion list, which also excludes tobacco, cannabis, thermal coal and oil sands, cluster munitions and mines, nuclear weapons, and violations of international conventions as defined by the Council of Ethics.

Two obvious reasons for PenSam’s list being longer relate to coal: it excludes both metallurgical and thermal coal, and has defined a very low threshold of only 5% for coal exposure while NBIM has a 30% threshold for coal. There are also more nuanced reasons – for instance, the list of companies that PenSam excludes based on worker rights is also longer than many other allocators, because it defines worker rights differently.

Countries

PenSam’s country exclusions are partly based on an ESG score, which ranges from 0 to 100.

Countries scoring below 30 are generally excluded, but in special situations we can decide not to exclude them…”

says Bek. Other exclusion categories are countries affected by certain sanctions and those on the EU tax havens list.

Some 19 countries, mainly in Africa and the Middle East, are excluded for a low ESG score: Afghanistan; Burundi; The Central African Republic; The Democratic Republic of Congo; Eritrea; Haiti; Iraq; Libya; Mali; Myanmar; Saudi Arabia; Somalia; Sudan; South Sudan; Chad; Turkmenistan; Uzbekistan; Venezuela and Yemen.

North Korea and Syria are excluded due to EU sanctions.

12 countries, which are nearly all island nations, are excluded for being on the EU’s “Tax haven” list: American Samoa; Anguilla; Barbados; Fiji; Guam; Palau; Panama; Samoa; the Seychelles; Trinidad and Tobago; US Virgin Islands, and Vanuatu.

The lists can change. In October 2020, Anguilla and Barbados were added to the EU list, while the Cayman Islands and Oman were removed.

Fair Taxation

Excluding tax havens can be seen in the wider context of PenSam’s policy on fair taxation, which also applies to companies that could be located and domiciled outside “tax havens”.

A group of Danish pension funds are working together to avoid aggressive tax structures. Of course, we want to avoid double taxation, but we also want to avoid situations where structures are designed to avoid tax altogether or pay very low rates….”

says Bek. Australian bank Macquarie has been excluded by a number of Danish pension funds since 2018 when it was found to be involved in a scheme to re- claim dividend tax multiple times. “PenSam has had no exposure to the dividend swaps scandal”, he confirms.

Engagement and Voting

Of course, exclusions are not the only part of PenSam’s ESG policy. Its active ownership approach also engages with companies. “Engagement takes place directly in Denmark, where we were very active in relation to the Danske Bank scandal. Outside Denmark, engagement is more indirect via groups such as Climate Action 100+ or Sustainalytics”, says Bek.

Pension funds do not always disclose the names of companies they are engaging with, but PenSam is transparent on this. Beyond its exclusion lists, PenSam’s “observation list” includes companies that PenSam is engaging with on various issues. For example, it is engaging with five companies, including Amazon, on worker rights; 22 companies including Swedbank on business ethics; nine companies including Volkswagen on climate and environment; 30 companies including Volvo on human rights; 20 companies including US tech giants Alphabet, Apple, Facebook, Microsoft on tax; and seven companies including Nestle on child labour in the cocoa industry.

Proxy voting is also actively pursued. ISS vote proxies on behalf of PenSam, in line with PenSam’s Principles for Voting, and report this back on the PenSam website….”

Impact Investing

As well as avoiding “negative” activity, PenSam is promoting “positive” activity through an extensive portfolio of impact investing, including infrastructure, green bonds, loans to green projects, and a Danish government sponsored fund involving 7 Danish Pension Funds. PenSam has also set a target of 10% climate related investments by 2025.

External Managers’ Scoring System

PenSam’s external managers do not necessarily need to meet every single aspect of its own ESG policies. PenSam ranks external managers on a scale of 0 to 60, based on their responses to 15 questions, with a maximum of 4 points per question. For instance, being a signatory of UNPRI would score 4 points in response to one of the questions. Managers should score at least 30, which in practice means their policies may be less extensive and thorough than PenSam’s own policies, but the emphasis is encouraging managers to improve their policies. Managers falling below 30 are given two years to get back above 30 before PenSam would redeem from them.