By Dr. Martin Dietz, Fund Manager, Head of Diversified Strategies, LGIM

Low interest rates across the Eurozone have focused investors’ attention on improving risk-adjusted returns. As an essential step, fully embracing diversification must be at the top of everyone’s mind. While diversification benefits are much discussed, we believe that many portfolios are still overly reliant on domestic assets and on equities.

One explanation for these biases may be that a more diversified portfolio often becomes more complex and expensive to manage. Outsourced solutions such as multi-asset funds can help in this regard.

Another challenge is that while the concept of diversification is well known, there isn’t a widely accepted means of implementing it in practice. On the contrary, many researchers have come up with different models, rules, and shortcuts for diversifying portfolios.

These proxies tend to run into one immediate hurdle: the complexity of financial markets. Asset classes do not follow normal distributions or conform to historical patterns, and the relationship between asset classes is always changing through time.

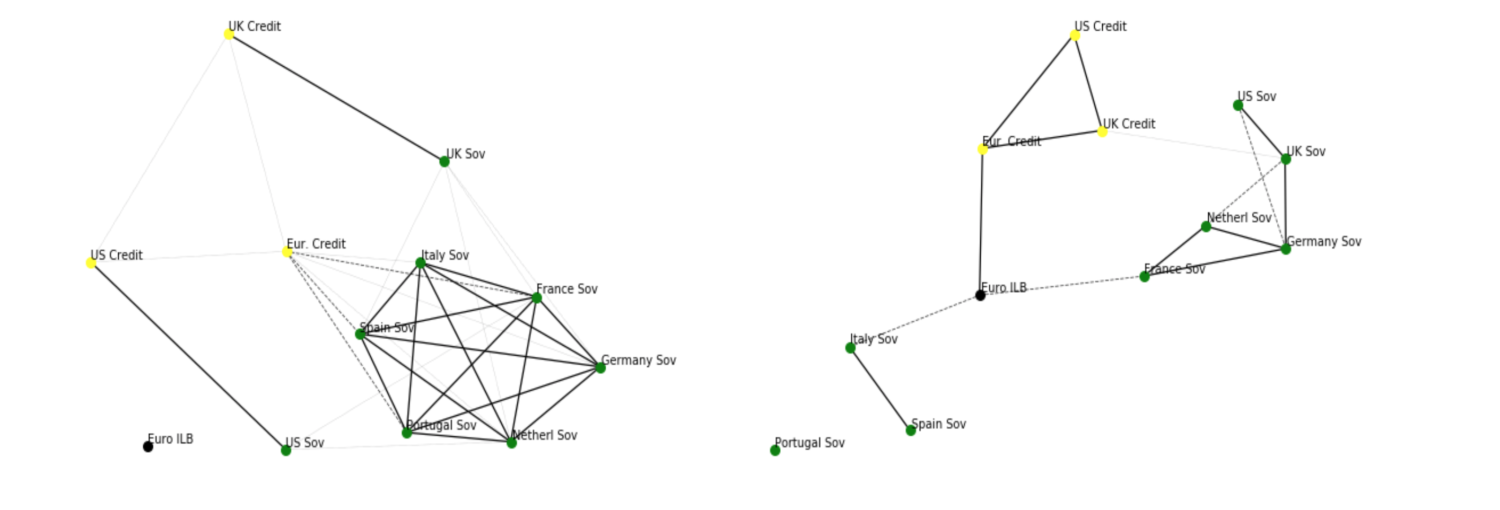

Correlation matrices are one way of showing the dependencies between asset classes, and we can visualise this information in correlation galaxy charts that plot highly correlated asset classes in close proximity to each other and uncorrelated ones further apart. Particularly high correlations are emphasised with dotted, solid or bold lines.

For example, Figure 1 illustrates how the relationship between European bond markets has changed over time. Between 1998 and 2007, they looked highly correlated – as if there was no benefit in diversifying among them. The European sovereign credit crisis, of course, laid bare the hidden underlying risks as peripheral Euro sovereign risk emerged.

Figure 1: Correlations between European sovereign credits before the crisis (1998-2007, LHS) and after (2009-2018, RHS)

(Source: LGIM analysis)

So while historical correlations can help us to identify patterns and draw some initial conclusions, we cannot rely on data from the rear-view mirror alone. We need to augment that information with our own expert knowledge and forward thinking.

Three steps to better risk management

While many investors have incorporated some degree of diversification into their portfolios over the past few years, we believe that there is still room for further improvement. This can be implemented not only in terms of the number of and selection of diversifying assets within a portfolio, but also in the weight given to those diversifying asset classes.

Despite the complexity of the data, our research suggests that there are three pragmatic, qualitative steps to help investors move towards a more diversified portfolio. We employ these alongside more rigorous analysis, but in our experience they can also help investors reach better outcomes if used in isolation.

1. Diversification by asset class and within asset classes

The rationale for allocating to additional asset classes is that they can provide exposures to return sources that are different from the equities and high-quality bonds of a conventional balanced portfolio. There isn’t a single “magical” asset class that will transform a portfolio; diversification is about adding a multitude of different exposures.

Beyond the quantitative analysis, understanding the underlying driver of returns is helpful too. For example, while high yield is linked to corporate balance sheets and therefore equities, it can perform well in market environments different from those favourable to stocks. Real assets, whether accessed as direct investments or through listed alternatives, can meanwhile provide exposure to physical assets with typically stable and broadly inflation-linked returns.

2. Diversification by geography

We believe that regional diversification should be the second pillar of an institutional portfolio, and we are particularly interested in managing regional economic and political risks. Most of this is related to equities, but investors should not forget the exposures they obtain through various other asset classes, such as sovereign credit risk.

When we design a regional allocation, we pay particular attention to the following three considerations:

- First, we want to avoid the traditional home bias of many investors; global exposure provides a portfolio with protection against decelerating Eurozone growth or local political risks.

- Second, investing into generic global or developed market indices often results in a large exposure to North America given the large size of US capital markets, which may expose a portfolio to a narrow set of economic or political risks that we want to minimise.

- Third, we want to increase the allocation to emerging-market countries from benchmark defaults given their market capitalisation is small compared with other measures of their importance such as their GDP, growth, and population.

3. Currency risk management

An additional issue when diversifying assets globally is that doing so leads to higher exposure to foreign currencies. This naturally invites the question of what level of currency hedging European investors should implement. Opinions on currency hedging differ widely, and the total asset exposure, risk appetite and investment beliefs will each play a role as well. But we believe that investors should consider their overseas currency exposure and hedging decisions as part of their overall portfolio construction, not just on an asset class by asset class basis.

Currency exposure can provide enhanced diversification, act as a hedge against tail risks, and offer additional returns. Exposure to safe-haven currencies such as the US dollar, Japanese yen and Swiss franc, for example, tends to mitigate risk in market downturns. Foreign currency exposure can also provide straightforward protection against any Eurozone-specific risks. Finally, high-yielding currencies – emerging-market currencies in particular – have historically generated attractive risk-adjusted returns for investors.

No panacea, but a time-tested improvement in portfolio efficiency

While there is no panacea when it comes to managing the effect of market volatility, we believe the simple steps we have laid out above can help European investors improve the efficiency of their portfolios.

Diversification is crucial to providing a portfolio with a multitude of exposures that should help to produce returns in a broader range of market scenarios and reduce the portfolio’s dependence on the equity market’s performance alone. Diversifying can also assist in providing natural risk hedges, for example through exposure to a safe haven like the US dollar. Finally, diversification should make a portfolio more efficient and investors can use these gains to boost their expected returns or to reduce risks.