By Aviva Investors Team

Recent events have highlighted the importance of the environmental, social and governance characteristics of real asset investments – not only as part of COVID-19 recovery programmes, but also as a way of futureproofing portfolios.

In the midst of a global pandemic, Apple announced one of the corporate world’s most ambitious environmental blueprints – to reduce the climate impact of every Apple device to net zero by 2030. The plan involves cutting 75 per cent of the company’s existing carbon footprint, not only for its own business but also across the manufacturing supply chain and product life cycle.1 The remaining 25 per cent will be removed via carbon capture and storage projects, including investments in forestland, mangroves and other natural ecosystems, as well as measures to offset emissions.

The programme, which aims to meet a net-zero goal two decades before the target set by the Intergovernmental Panel on Climate Change (IPCC), addresses levels 1, 2 and 3 emissions. This includes emissions from the day-to-day operations of the company, as well as its upstream suppliers and downstream customers. What stands out is the company’s focus on reducing the carbon intensity of the infrastructure and real estate upon which its devices are built, operated and serviced. As Apple expands and needs more stores, offices and data centres, this is no easy task.

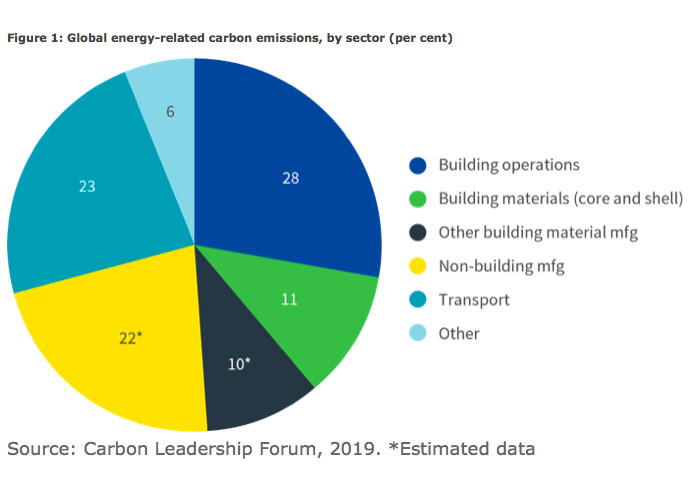

Globally, 39 per cent of all energy-related carbon emitted comes from building and construction…”

according to the World Green Building Council.2 Operational emissions – mostly from heating, cooling and lighting buildings – account for about 28 percentage points. Commercial property landlords and tenants can cut energy use by shifting to non-fossil fuel sources, by using less energy, or both. The transition away from fossil fuels towards renewable energy has long been part of corporate plans to reduce carbon.

German engineering conglomerate Siemens, for example, uses a mix of renewable energy, combined heating and power (CHP), and storage systems, supported by advanced energy management, to lower emissions of its production facilities and office buildings.3

Opting for materials, logistics and construction methodologies with less carbon impact can also help. ‘Embodied’ carbon emissions account for the remaining 11 percentage points of emissions from the building and construction sector worldwide (see Figure 1). By comparison, air travel accounts for about 2.5 per cent of global carbon dioxide emissions.4

“The transition to low carbon will define the real estate sector over the next decade. There’s a window of opportunity as we reconfigure our assets in response to the COVID-19 crisis, where delivering healthy and low-carbon products into the market can meet the needs of tomorrow’s occupiers,” says Ed Dixon, head of environmental, social and governance (ESG) for real assets at Aviva Investors.

When COVID-19 began spreading globally earlier this year, the concern was that ESG considerations would take a back seat as individuals, governments and companies focused resources on battling the health crisis. In fact, the opposite may be happening.

On announcing Apple’s 2020 Environmental Progress Report in July, the company’s vice president of environment, policy and social initiatives Lisa Jackson said:

This year has offered humbling reminders that nature is bigger and more powerful than any one of us—and that our ability to solve worldwide challenges depends on historic innovation and collaboration….”

Whether through the UK’s ‘Build Back Better’ initiative or the European Union’s ‘Green New Deal’, ESG considerations have a central role to play in coronavirus recovery programmes worldwide. In this respect, one of the main sectors to be affected will be real assets. They are long term. They transform communities. And they are crucial to global economic growth.

“The nature of real assets means they will play a crucial role in preparing for future crises,” says Dixon. “ESG in real assets has gone beyond integration. It’s now about hard and fast results – results for clients, in terms of balancing risk and returns, and results for society in the form of resilient buildings and infrastructure.”

Here, we consider four areas set to shape the ESG agenda for real assets in the coming years: the path to net-zero carbon emissions; transformation of the workplace; increased focus on social impact; and the embedding of ESG considerations throughout the life cycle of investments.

Mapping net zero

Efforts to mitigate climate risks worldwide centre on the 2015 Paris Agreement, which seeks to keep global temperature rises this century less than two degrees Celsius above pre-industrial levels and, if possible, to 1.5 degrees. To achieve this, the world’s carbon emissions need to reach net zero by 2050, according to the IPCC.

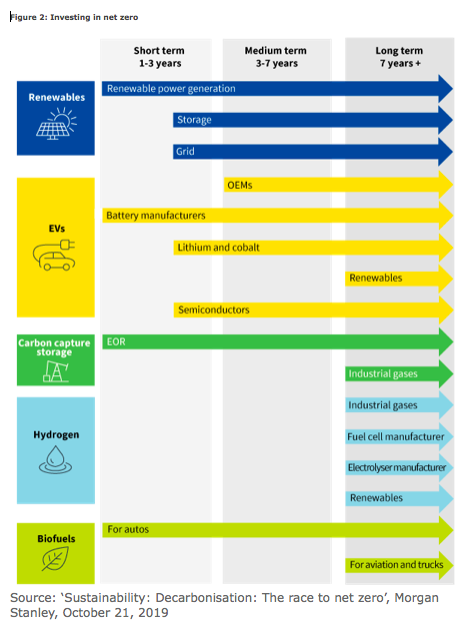

Nearly a quarter of the world’s top corporations have committed to specific climate action targets, representing a fourfold rise since the Paris Agreement was signed.6 Besides companies such as Apple, local and national governments worldwide have set their own targets. The UK, for example, in 2019 became the first nation to pass legislation requiring it to be net zero by 2050. As governments and corporations look at ways to reduce emissions, investment portfolios will need to align (see Figure 2).

Bringing a real estate portfolio in line with net-zero targets will have “profound implications”, according to Dixon. “It means only buying assets where you have full confidence they can be decarbonised in time, and refurbishing, redeveloping or disposing of everything else in your portfolio that isn’t being managed in line with your pathway to net zero.”

In August, a consortium of around 70 members of the Institutional Investors Group on Climate Change (IIGCC) released its net-zero investment framework, a proposed plan for harmonising investment decisions with the Paris Agreement. Once finalised, the framework should encourage institutions to “implement or explain”.7 The proposal initially includes sovereign and corporate bonds, equities and real estate, with infrastructure among other the asset categories to follow.

“The net-zero goal will have huge implications for many of the real assets we invest in,” says Laurence Monnier, head of quantitative research for real assets at Aviva Investors.

The three main challenges to reach net-zero emissions are to decarbonise the heating and cooling of buildings; decarbonise transport; and decarbonise power…..”

The scale of the required energy transition is enormous. In the UK, for example, about 300,000 terawatt hours of electricity are consumed annually. The expectation is for consumption to double in the next 30 years while net carbon must fall to zero.

“We need to produce twice as much electricity and take all the carbon out of it,” Monnier says. “Today, most electricity is generated by thermal plants that create carbon.”

The growth of renewable energy alone will not be enough to meet this need, particularly as wind and solar are intermittent – and may not be generating when demand is at its highest. Achieving net zero will require significant investment to decarbonise both power and transport. The government will need to provide the right framework to support investments in both existing and developing technologies such as heat pumps, battery storage, carbon capture and storage (CCS) or hydrogen. Incentives could include higher carbon prices, as well as new regulation.

The implication of this are significant for real asset investors, in terms of the life of existing investments and new opportunities….”

Work, at a distance

COVID-19 is also shifting the investment landscape for real assets. One enduring legacy of the pandemic could be a fundamental change to working practices, not only affecting the economics of real asset portfolios but also what it means to be a responsible asset owner. Aligning investment objectives with ESG responsibilities will require “deeper engagements with occupiers and the communities in which we’re investing”, Monnier says.

Health issues remain an acute area of focus of business, so improving the safety of the working environment will be crucial. Office buildings will likely accommodate fewer people on average as more employees work from home. Yet higher peak periods could be expected if more employees are coming into the office at the same time to seek face-to-face interaction and collaboration with colleagues, still an important ingredient to fuel the knowledge economy.

Companies may have less people in central offices, but they will need more space per person to protect them, so it is unclear whether office buildings will necessarily shrink.

A reconfiguration of the way space is organised and managed is required…”

says Sam Carson, director of sustainability at Carbon Intelligence, a London-based consultancy that advises companies on how to reduce their carbon footprint.

Additional ventilation may be needed, so central heating or air conditioning systems will likely have to work overtime. Along with lower occupancy, the rate of kilowatt hours of energy use per person will likely climb. Meanwhile, residential energy use is also up because more people are working from home.

“In my own company, probably about half of all employees will need permanent workstations in the future. But at the same time, the office needs to be more flexible to adapt to how people are using the space,” says Carson.

The design of buildings will need to change dramatically, and we could also see locations shift to more satellite hubs rather than central offices….”

Upon returning to the office, occupiers are likely to expect more of a destination for their staff, accelerating the demand for modern, flexible office space with stronger environmental credentials such as energy efficiency, state-of-the-art digital technology, and greater emphasis on health and wellbeing, Dixon adds.

London office buildings with the highest levels of sustainability certification already command a premium relative to the average rent while also benefitting from lower vacancy rates 24 months after completion, according to JLL.8

With real assets portfolios likely to be reconfigured to adapt to this new world, asset owners share the challenge of managing partners and suppliers responsibly. As workers return to support the construction and operation of buildings and infrastructure, the wellbeing of the workforce has become critical. Many supply-chain roles in construction, cleaning and security are exposed to health and safety risks, as well as pay that is at or just above the national minimum wage.

Being a real asset investor comes with responsibility. We must commit to creating safe and fair employment in the properties we manage, construction projects, and in the supply chain….”

Dixon says. “Whether people are paid on time, whether they are paid fairly and the conditions in which they are working are crucial to create stability in society and protect the rights of individuals. As an asset manager, there are levers we can pull to create change.”

The rights of employees and communities will likely hold larger implications for real asset investors – not only in terms of the workplace, but also the workforce. As responsible investors, asset owners can no longer be faceless bystanders – they have to become an integral part of the change required. Dixon says: “Can we capture the spirit of response to this health crisis to build the future we need to deal with the more long-term crisis of climate change and social inequality?”

Social impact: Vital, but hard to measure

However, the aims of the ‘S’ don’t always align with that of the ‘E’ and ‘G’ in ESG. Therefore, asset owners need a consistent process to guide how they balance the trade-offs in their investment decisions.

“Questions around the social aspects of ESG are becoming more important,” says Stanley Kwong, ESG associate director, real assets, Aviva Investors.

There is a lot of discussion about how to measure social improvements as part of an investment, which is challenging because social metrics are less quantifiable compared to environmental improvements….”

Such difficulties have led more institutional investors to turn to the Sustainable Development Goals (SDGs) to target specific ESG goals. They include pension funds such as the $563 billion Stichting Pensioenfonds ABP from the Netherlands, the $200 billion New York State Common Retirement Fund and Denmark’s $52 billion PKA.9 According to the United Nations Principles for Responsible Investment (UNPRI), the recent push to use the 17 SDGs10 to set investment targets has the potential to help real asset investors obtain much better clarity on how they are shaping outcomes.11

In assessing a railroad construction project in Sub-Saharan Africa, for example, weighing the trade-offs between the impact on the environment versus the potential to bolster the economy is fraught with complexity.

“In this particular case, the net positive effects of a new railroad development to support the economy and trade and contribute to social mobility outweighed concerns for the impact to the environment,” says Kwong. Furthermore, additional clauses may be added to the terms of the transaction to reduce environmental risks.

“If the risks are well understood, then it’s possible to analyse it correctly, engage the right stakeholders and put mitigating steps in place,” he adds.

You can futureproof your ESG risk, but you need to first determine what is the actual risk exposure, and second, what is your mechanism for mitigating that risk….”

Asset owners and investment managers are beginning to use the SDGs to set targets for asset allocation or other elements of asset management.12 Some governments are also using the SDGs to help shape their infrastructure planning and project design requirements. “This should encourage investors to align their own internal processes to position themselves better in government tenders for new infrastructure projects,” according to the UNPRI.

Incorporating ESG through the lifecycle

Understanding ESG characteristics is a dynamic process, requiring both top down and bottom up approaches. For real assets, this takes on an even more complex dimension given the longer timeframe of investments, which may stretch decades.

To truly invest for the long term, investors will need to embed ESG in their investment decision-making process – from origination through to the investment management stage and finally, responsible divestment or disposal, says Dixon.

Allocating more capital to sustainable projects to focus on mitigating climate risk is a start, but investors should also consider the social aspects, such as steps to bring about ‘a fair climate transition’, so employees and communities are less likely to be economically stranded….”

As with traditional financial analysis, ESG impact will differ according to the nature of project, sustainability credentials of the company and where the investment sits in the capital structure, among other factors, Kwong says.

Contrast two projects, one involving a real estate long-income transaction for a UK gas operator and the other a self-storage facility for real estate debt. In the first instance, the environmental risk of the sector is an obvious consideration. Would an investment in gas fit into an investor’s net-zero ambitions? What is the company doing to reduce emissions? What is the social dynamic with the surrounding communities? Those sorts of questions are key.

In the second case involving a self-storage facility, the main driver of ESG risk will likely be the building itself. Therefore, one way of mitigating the carbon risk may be to negotiate a green clause, which allows incentives for reducing emissions by installing solar panels or improving energy efficiency.

That also improves the ESG credentials of the underlying asset, adding value for investors, From these two transactions, you can see that what you need to do in terms of futureproofing the portfolio is completely different….”

Once assets are added to the portfolio, active ownership helps mitigate ESG risks and maximise value, Dixon says. Estimates suggest about 90 per cent of European real estate was built before 1990, likely with poor-quality insulation, outdated heating systems that rely on gas, and poor air quality management.13 Yet according to JLL research, office buildings that have the highest levels of sustainability certification command significant rental premiums of at least ten per cent above average.14 This presents a significant opportunity to refurbish assets and realise the uplift in rents and asset value.

“There is a lot of work to be done in the asset management phase, and that’s where a lot of value is generated in real estate,” adds Monnier. “Architects are now calling for more effort to be devoted to upgrade existing buildings rather than constructing more efficient new facilities, given the latter’s higher carbon footprint.”

Using more renewable energy or reducing the amount of energy being used, for example, reduces carbon emissions. Sensors may be installed to further add efficiency by automatically adjusting temperatures according to times of the day when the space is occupied. Explains Dixon:

The point is not to let the assets sit there dormant, being managed by someone else, but to actively manage them to minimise the impact to the environment – and value to the occupier – over the lifetime of the assets…”

When it is time to divest or dispose of assets at the end of its lifecycle, ESG criteria also need to be carefully considered. Asset owners have a responsibility to minimise the impact of asset disposals on customers, employees and wider society. In cases where assets are sold to another investor, due diligence will be key. ESG liabilities may extend far beyond the point of divestment.

“We have to look critically at who we sell assets to,” Monnier says. “It goes back to knowing your customer.”

As Apple has demonstrated, and others will likely follow, COVID-19 has offered a stark glimpse into the potential impact of the climate crisis. Ten years ago, an investment in a coal-fired plan, for example, may have been financially prudent even if the non-financial environmental risk was high. Fast forward to today, however, and the case to invest in coal carries far more financial risk. It illustrates that a non-financial risk can morph into a financial risk over time.

Without absolute certainty on what the future holds, the best way to futureproof portfolios is to constantly scrutinise the potential for change and make sure you are prepared for it.

For more insights in this space, visit Aviva Investors

References

- ‘Apple commits to be 100 percent carbon neutral for its supply chain and products by 2030’, Apple Inc., July 21, 2020

- ‘Global Status Report 2017’, World Green Building Council, December 11, 2017

- ‘Five companies reducing their carbon footprints’, Impact Hub, August 1, 2018

- Hiroko Tabuchi, ‘Worse than anyone expected: air travel emissions vastly outpace predictions’, The New York Times, September 19, 2019

- ‘2020 Environmental Progress Report’, Apple Inc., July 21, 2020

- ‘Deeds not words: New research reveals the climate action of fortune global 500 companies’, Natural Capital Partners, September 18, 2019

- ‘Consultation: Net-zero investment framework’, IIGCC, August 5, 2020

- ‘Sustainability and value in central London’, JLL, 2019

- Sarah Rundell, ‘Investors continue to align with SDGs’, Top1000Funds.com, August 18, 2020

- 10.‘About the sustainable development goals’, United Nations, 2020

- 11.‘Bridging the gap: how infrastructure investors can contribute to SDG outcomes’, United Nations Principles for Responsible Investment, 2020

- 12.Ibid

- 13.Irati Artola, Koen Rademaekers, Rob Williams, Jessica Yearwood, ‘Boosting building renovation: What potential and value for Europe’, European Parliament’s Committee on Industry, Research and Energy., October 2016

- 14.‘Sustainability and value in central London’, JLL, 2019