By Simon Wallace, Global Co-Head of Alternatives Research and Strategy at DWS

Having entered this downturn in a strong position, and with the support of exceptional action from government and central banks, values have so far fallen less than expected. However, this is no time for complacency.

______________________________________________________________________________________________________________

While we continue to see attractive long-term opportunities, the coming months will be challenging.

Urban logistics pushing rents higher

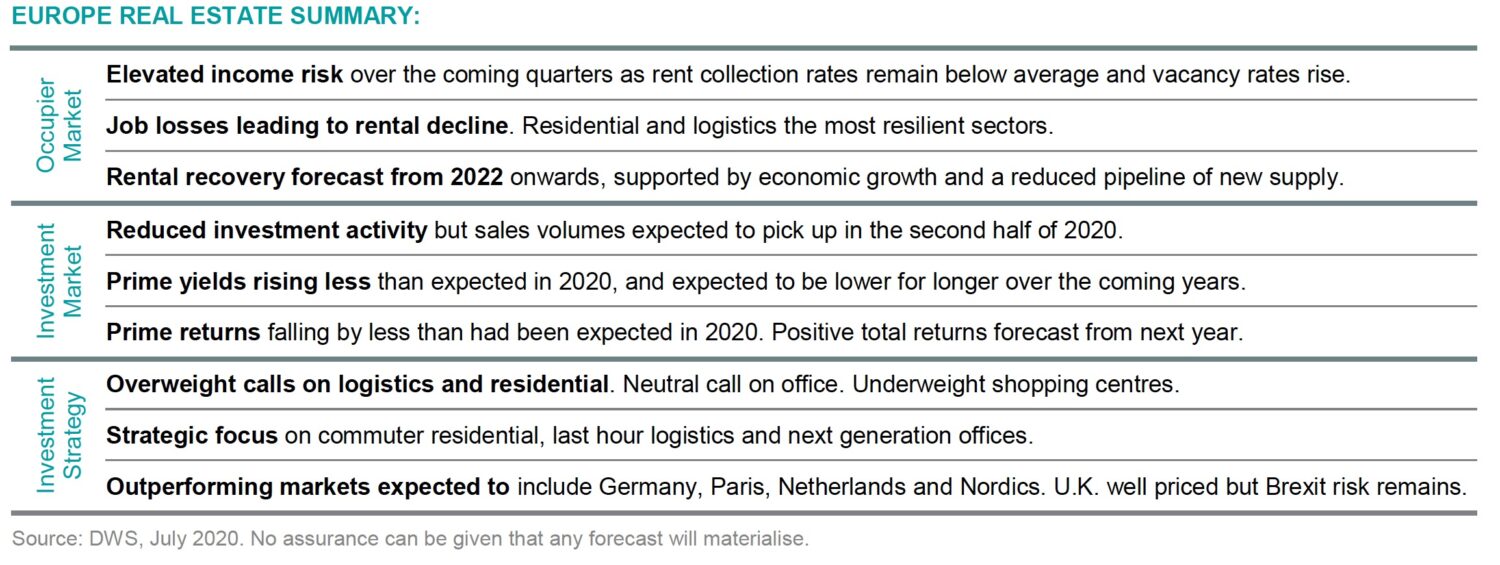

We remain concerned about parts of the occupier market. The real estate market started this year on the front foot, but with unemployment rising and millions of employees still supported by furlough schemes, we do not see an immediate increase in occupier demand. However, the picture is far from uniform. Prime office rents are forecast to fall by 6% this year, but residential and logistics look far more resilient, particularly urban logistics where surging demand for home delivery is pushing rents higher. In contrast, an already weak retail market remains under considerable pressure.

Overall we expect all property prime values to fall by around 10% in 2020. This is an improvement on our March forecasts, and reflects our view that yields will not rise by as much as we had originally feared. While transaction volumes are down compared to a year ago, there remains a large amount of dry powder ready to invest. And with recent improvements in equity and bond markets, real estate pricing is once again looking relatively attractive. Assets with a strong income and a long-term growth story continue to attract considerable attention and may even see yield compression.

Looking further ahead, the market is forecast to enter its recovery phase from next year onwards. Initially led by yield compression, we expect returns to turn positive in 2021 before accelerating into 2022 with the return of rental growth.

The Nordic region offer attractive risk-adjusted returns

We see the most attractive risk-adjusted returns in Core European markets such as Germany, Paris, the Netherlands and the Nordics. London also stands out as a top pick, although there are clear short-term risks around Brexit. Logistics and residential remain the top performing sectors, with attractive opportunities across almost all major cities. We’re more cautious on office, and while prime CBD demand should improve with the jobs market, structural changes are increasing the risk of obsolescence – something that will continue to weigh heavily on the outlook for shopping centres.

The European market has weathered this storm better than many of us were expecting. However, the storm is not over yet. While it’s right to prepare for the recovery, risks remain elevated. With this in mind it is important we retain a focus on sustaining current income while also looking to benefit from long-term structural drivers.