By Lupin Rahman, Global Head of Sovereign Credit, PIMCO

ESG criteria are an integral part of our sovereign ratings analysis and provide important context to our assessment of a sovereign’s creditworthiness. We believe incorporating ESG factors into traditional sovereign analysis helps the identification of credits with potentially lower long-term credit/higher default risk, as well as countries with positive and/or negative ratings momentum. Both are material to the evaluation of sovereign default risk in the medium term and the price of sovereign credit risk in the near term.

A key challenge when considering which ESG factors to consider in sovereign analysis is the issue of potential latent risks, which tend to manifest in the long term and often have indirect effects on creditworthiness. And, when they do, they can have significant binary effects. The Arab Spring in 2011 is an example: Extremely high levels of youth unemployment, income inequality and limited political voice coexisted for decades in what was essentially a “stable disequilibrium.” These initial conditions sparked a sudden and full-blown movement for social and political change across the region. A latent risk emerged rapidly – with profound effects on sovereign credit.

The investment process

PIMCO seeks to uncover and analyse latent risks in sovereign credit via a multifaceted approach, including:

- Proprietary ratings model: PIMCO’s proprietary sovereign credit ratings model incorporates many quantitative ESG indicators, which include near- and long-term drivers of credit risk, as well as variables that may be more slow-moving and have more diffuse effects. These include (amongst others) measures of political stability, voice and accountability, rule of law, income inequality, literacy, labor market indicators and health indicators. Together, these ESG variables have a combined weight of approximately 25% in the model and as such directly affect our absolute sovereign ratings. They also contribute to changes in our ratings outlook if there are large shifts over time.

- Third-party checks: PIMCO’s proprietary sovereign ratings are complemented by analysis from credit rating agencies, international financial institutions such as the International Monetary Fund, and standalone sovereign consultants. Where there are differences, we consult with these sources to assess what is driving the difference and what underlying assumptions are being considered in the alternative sources of analysis. This is particularly important for latent ESG risks, which can have varying degrees of importance depending on the approach.

- Standalone ESG score: Complementing our sovereign ratings model is a standalone ESG score that includes a wider range of variables than the sovereign model. For example, it includes very slow-moving latent risks such as mortality and health indicators. It also includes indicators that may affect credit risk via indirect channels, such as labor market standards.

- Scenario analysis: Finally, we conduct country-specific scenario analysis to assess medium-term, more extreme risks. Risks assessed include those relating to political regime change, long-term debt sustainability, resource depletion and natural disasters. This analysis helps us identify what risks are material for investing, which sovereigns are most prone to them and what contingency plans they have in place.

We find that the combination of the sovereign ratings model, third-party checks, standalone ESG score and scenario analysis provide a better assessment of latent sovereign risks. The ratings model directly includes these risks in our credit assessment, the third-party checks and ESG score act as a flag for issues that are not explicitly incorporated in the ratings, and the scenario analysis provides a framework for thinking about the probability of these outcomes and the consequences should they occur.

The investment outcomes

This approach has helped PIMCO recognize potential latent risks over the long term and better manage left-tail risks (i.e., less likely events that could have major effects). It enabled us to navigate a challenging environment in the aftermath of the Arab Spring where the political economy of several countries in the region became more uncertain. It also helped us identify sovereigns where similar risks existed. Specifically, it shaped how we approached the social risks associated with the aftermath of the eurozone debt crisis. There we identified in advance the shift towards populist political regimes and the tensions this would create between the core and the periphery economies. As such we took a more cautious approach to adding European risk during the initial stages of the crisis.

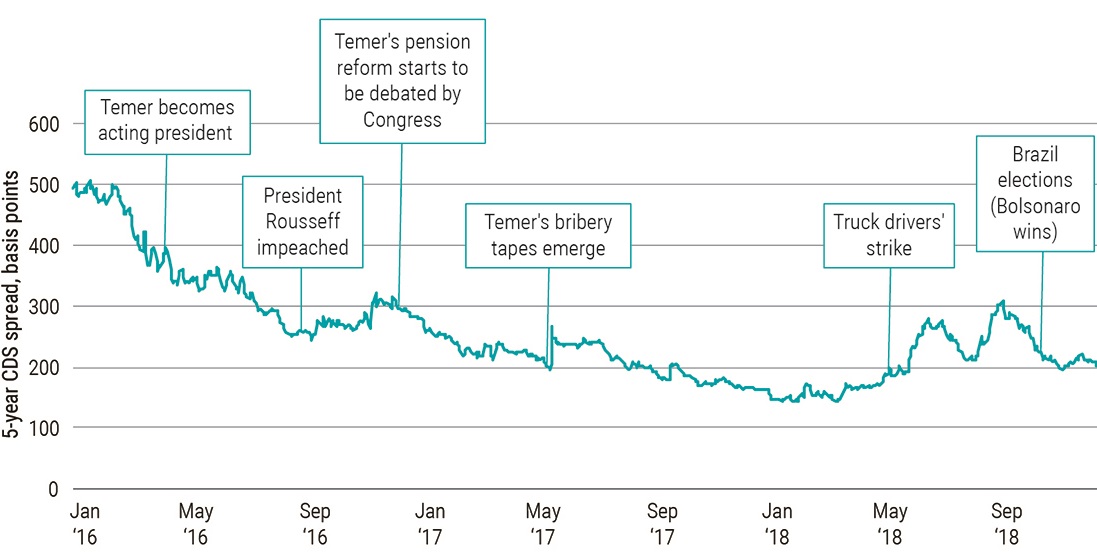

Our approach to latent ESG risks has also been a key input in our assessment of political regime changes across the globe including in Brazil, Mexico and Argentina, as well as helping assess where political regimes have remained in place despite these latent risks, e.g., South Africa and Russia. On a more micro level, focusing on events such as strikes, protests and riots have allowed a deeper analysis of government reaction functions that can directly affect sovereign credit risk, e.g., the fiscal concessions made in the aftermath of the truckers’ strike in Brazil made us more cautious on investing in the country as we discounted the chance of pension reform ahead of the October 2018 elections.

Source: Bloomberg and PIMCO as of 13 December 2018. CDS: Credit default swaps.

Key takeaways

The key takeaway has been to be proactive and continually reassess our investing and credit risk priors in our identification and assessment of latent ESG risks in sovereign credit analysis. While it can be tempting to overlook them given the bias towards near-term material risks, their binary nature and the potential for severe consequences can mean that ignoring them could result in overlooking big risks to portfolios and/or missing important investment opportunities.