By Jonas Wäingelin, NordicInvestor

Gold and silver are often thought of as commodities, but they are more than that. Ned Naylor-Leyland, fund manager and head of gold and silver at Jupiter Asset Management, explains why he believes gold has an important role to play in a well-diversified portfolio, and why this is best achieved through an actively managed approach, combining allocations to gold, silver and the shares of mining companies.

Why does it make sense to allocate to gold now?

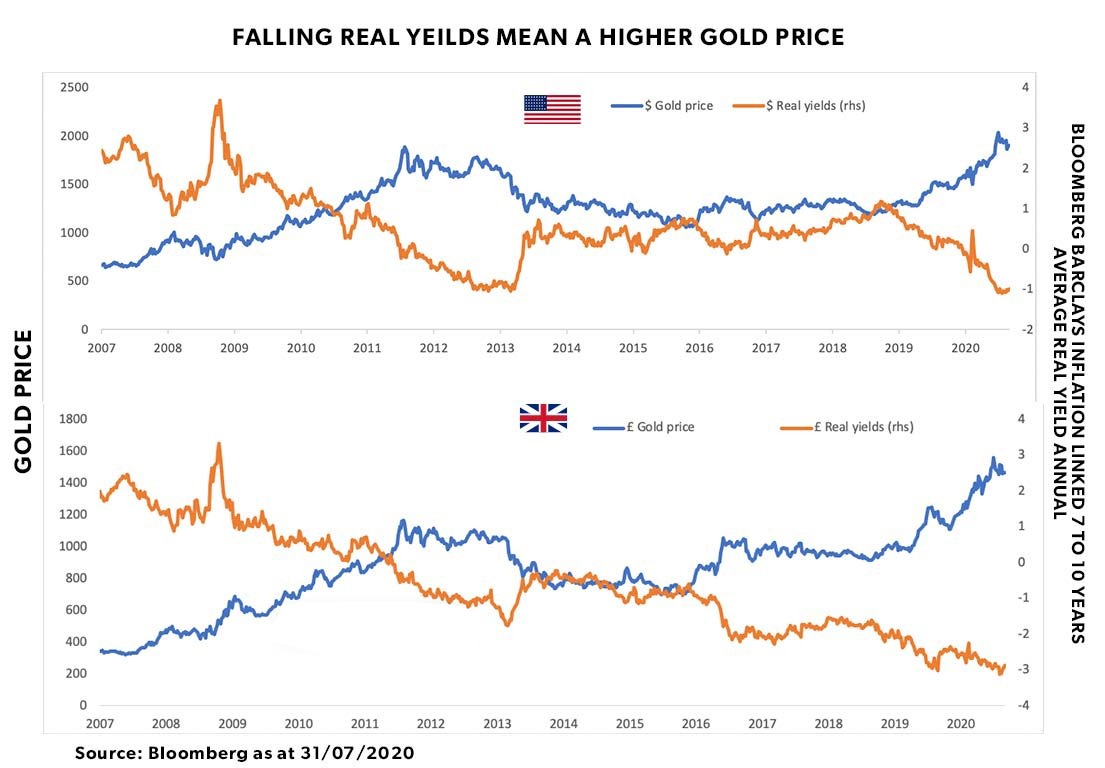

There has been a strong rally in the price of gold, from around US$1,500 per ounce at the beginning of the year to a record high just above US$2,000 recently. Despite this, many investors are still playing catch-up and are underweight monetary metals. Behind the rallies in gold and in silver are the commitment of the US Federal Reserve (Fed) to monetary loosening, the swelling of central bank balance sheets, and the spike in government spending, fuelling distrust of the US dollar. Negative real yields mean that many US Treasury bondholders face losses in post-inflation terms, which makes gold and silver attractive as stores of true value. We see this trend continuing, and it is an ideal environment for monetary metals.

Is gold an inflation hedge or deflation protection?

The gold price typically moves inversely to real interest rates – the rate of interest excluding the effect of expected inflation: in this way, it can help to defend a portfolio against the effects of inflation. Inflation is often hidden — making timing an allocation to gold difficult. Think about “Shrinkflation,” whereby products become smaller, but manufacturers maintain the price. This is a well-known phenomenon. It is harder to track than simple price rises but is a good example of how inflation can appear from “out of the blue.” While deflation exists in the monetary sphere, if you asked people on the street about their experiences with inflation, you would struggle to find anyone who thought their cost of living was going down. Academic studies show that 2-5% in gold, as a fixed allocation, is optimal for portfolio diversification purposes.

Why does it make sense to allocate to a fund with gold and silver and with mining companies?

Silver is currently trading in a mid-US$20s per ounce range, but it is worth remembering that in 2011 when markets were also in ‘do whatever it takes’ mode, silver reached US$50 per ounce. Gold and silver are siblings. It has been said that gold is the money of kings, silver that of gentlemen and gentlewomen. Silver typically increases in value faster than gold when precious metal prices are rising, although it declines faster when prices are falling. Therefore, it makes sense to increase exposure to silver when prices are rising and reduce when they are falling.

Taking exposure to shares in companies that mine gold and silver also offers the potential to generate superior returns when gold and silver prices are rising, as mining company shares tend to rise (and fall) more than the prices of the metals themselves. Mining services and equipment are deflating, and due to fiscal and monetary looseness we can expect spot gold and silver prices to continue to move sustainably higher. This is a powerful call option-like set up for gold and silver mining equities. Also, higher market prices for gold and silver have not yet been fully factored into valuations of mining equities Finally, the gold mining sector has seen around $20bn of mergers and acquisitions this year and this may well double in the next 3-6 months, driven by a crisis in depleting reserves among major gold miners.

Why an actively managed fund versus an ETF?

An actively managed approach may mean a small allocation to such a fund could offer similar potential benefits to a portfolio as would a larger holding in pure gold in, for example, an exchange-traded fund (ETF). Another reason is that governance matters. It is important to take exposure to bullion that is stored and traced to the highest global standards and take exposure to mining companies operating with the highest standards of governance and employee welfare. An actively managed fund can do this, but we do not believe an ETF can offer such assurances.

Are there other reasons to allocate to gold?

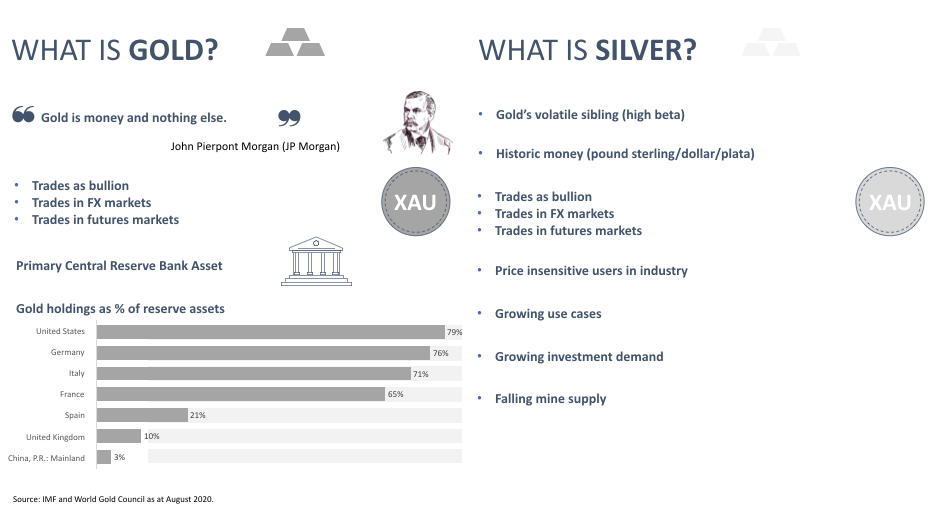

Gold is the traditional hedge used by central banks and institutions to protect against both inflation and risk in markets. Some of the world’s most important central banks, including the US and Germany, hold a significant proportion of their total reserves in gold. Also, gold is not political currency in that it is not issued by a central bank or government. In contrast, the US dollar is highly politicised, and its privileged role in the global financial system is increasingly being questioned. Some countries, including China, are looking to fill the role historically played by the dollar, for example, to buy oil. If this trend continues, the importance of the role of gold could grow.