By Dáire Dunne, CFA – Portfolio Manager, Wellington Management

One of the main arguments for investing in emerging markets (EM) equities over the past 20 years has been the above-average economic growth in EM countries. Yet this growth advantage has begun to fade as EM policymakers have switched their emphasis in recent years. Rather than simply pursuing growth at all costs, they are now focusing on the broader goal of economic development, which is more concerned with the quality and durability of growth, along with greater social cohesion and environmental sustainability. This shift in emphasis is enhancing productivity and encouraging growth in new industries.

Yet markets tend to be better at assessing near-term dislocations (such as the impact of a sudden fall in the oil price on EM oil-exporting countries) than appreciating structural changes. I believe that understanding the structural changes associated with the emphasis on economic development will be key to tapping the potential of EM equities over the coming decades. Furthermore, our research indicates that EM stocks linked to development trends are less volatile, as they are driven predominantly by local policy and domestic demand and are less sensitive to global forces, such as trade sentiment and tariffs. Certainly, they have held up relatively well during the recent market weakness caused by political uncertainty, macro volatility and trade tensions.

In my view, there are four key forces of structural change related to economic development:

- Greater inclusiveness, broadening the range of beneficiaries of economic progress. This brings wider access to health care, education and sanitation, reduced inequality and improved life expectancy.

- Sustainability, as available resources are used with greater consideration for future generations and the environment. This results in improved recycling, water and waste management, energy efficiency, alternative energy sources and testing and diagnostics.

- Improved living standards, to ensure stable progress for the whole population. This leads to changes in how consumers spend their time and money.

- Enhanced productivity, increasing the efficiency of all available factors of production. This is evident in the use of technology, promotion of innovation, support for training/higher education and institutional reform.

These structural forces can materially impact a country’s prosperity, leading to a broader range of industries, greater innovation and knowledge sharing, a wider variety of goods and services and reduced inequality. Typically, they also result in deeper financial markets, with more listed companies, and a favourable environment for profitability ― and thus rich investment potential.

I believe that markets are underappreciating the political determination to make economic progress more stable and inclusive. For example, even as growth rates across EMs have slowed, we have seen continued increases in health care and education spending, the market share of renewable energy and access to electricity and clean water.

Consumers push for change

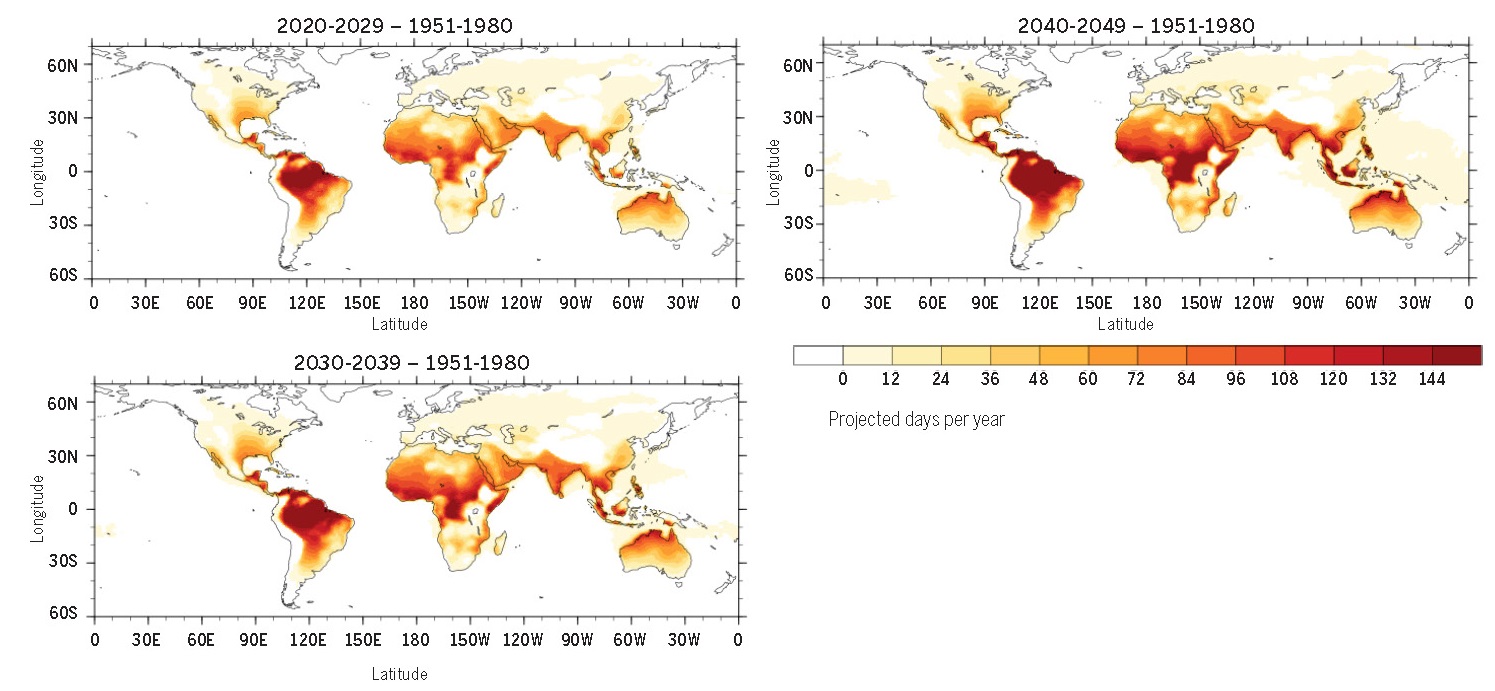

The move towards economic development is coming not only from policymakers but also from consumers concerned about environmental issues. This is particularly evident with climate change. Wellington has conducted analysis in collaboration with the Woods Hole Research Center, one of the world’s leading independent climate research institutes, on the expected increase in extreme heat patterns globally. The below shows the disproportionate impact on the emerging world. Regions in darker colours may suffer not only higher temperatures but also more severe droughts.

EMs are likely to suffer a disproportionate share of climate-related impact

Additional days per year in the danger zone

World based on the 1951 – 1980 reference period

Danger zone is defined as the National Weather Service Heat Index danger and extreme danger zones, which include heat index values above 103º Fahrenheit. Source: National Weather Service. The target data is hypothetical. No assurance or guarantee is made that any target data can or will be achieved. Actual experience may not reflect all of the data or may be outside stated ranges.

The Pew Research Center, which publishes annual Global Risk reports, has noted that climate risk has for several years topped the list of worries of EM citizens. These concerns have put pressure on policymakers in countries as geographically, climatologically and politically diverse as China, India, Indonesia, Brazil and Poland to respond aggressively by incentivising greater energy efficiency, shifting to less carbon-intensive energy sources, promoting greater recycling and adopting more efficient waste management. I expect these pressures to persist and even increase in the years ahead, further entrenching the drive towards economic development.

From backward-looking benchmarks…

But will a passive or benchmark-relative approach get investors sufficient exposure to the likely beneficiaries of the development drive? The sector compositions of traditional EM benchmarks largely reflect the winners of the rapid-growth phase of recent decades, with large weightings to technology hardware, financials, materials, energy and exporters. By contrast, the sectors which stand to benefit most from the four forces of structural change are significantly under-represented.

Take health care as an example. EM demand for health care services and pharmaceuticals looks set to increase substantially over time, given ageing populations, the rapidly growing middle class, the prevalence of chronic disease and the current lack of preventive treatment. Policymakers recognise the importance of delivering on that demand, and I expect health care’s contribution to overall economic activity to increase substantially. Yet the sector currently accounts for only 2.6% of the MSCI Emerging Markets Index.

An increased tilt towards development-related sectors could also bring greater diversification to portfolios. Emerging markets were once prized for their diversification benefits. Yet their correlation with developed markets has more than doubled over the past 30 years, driven partly by the dominance of globally oriented sectors such as energy, materials and financials, which are related more to growth than to domestic economic development.

…to forward-looking portfolios

These beliefs led us to construct a portfolio focused solely on economic development, using individually constructed themes. We seek to generate significant alpha at the stock level by distinguishing between the “winners” and the “losers” of these trends, which lead to significant creative destruction.

The result is a portfolio which we believe represents the core allocation of the coming decades. It looks very different from traditional market-cap-weighted benchmarks and so may complement core EM exposures. This approach directs our research towards areas where we expect to find future outperformers that should thrive on the disruption driven by economic development.

For example, infrastructure and logistics is an investment theme at the intersection of many powerful forces in EMs, such as demographics, urbanisation, productivity and ecommerce. The physical movement of capital between and within countries requires sustained investment over decades and is creating a growing set of opportunities. This theme is among the broadest we observe across EMs – witness the “Build, Build, Build” programme in the Philippines, increased spending on inter-island connectivity in Indonesia, China’s “One Belt, One Road” investment and India’s Eastern and Western Dedicated Freight Corridors. Despite this widespread commitment to investment from the public and private sectors, the theme remains a small allocation in broad market indices and thus, by default, in many investors’ portfolios. We believe this represents a missed opportunity.

Conclusion

As the EM growth tailwind fades and the focus shifts to economic development, I believe there is a wide variety of attractive investment opportunities for unconstrained investors. A thematic approach focused on the four forces of structural change can help to identify these opportunities and potentially generate attractive risk-adjusted returns while complementing existing broad-based EM exposures.