By Jonas Wäingelin, NordicInvestor

EMD for both the good and bad times

The reasons why investors like emerging market debt (EMD) in the ‘good times’ are well known. The asset class offers the attractive combination of access to high economic growth, strong fundamentals, and higher yields than its developed market equivalents.

But Alejandro thinks it’s important that investors consider the asset class in the ‘bad times’, too. A more challenging global backdrop, including a combination of ongoing trade tensions and slowing global economic growth, is not a reason to run away from EMD. While there is often a ‘knee-jerk’ reaction from investors in these conditions, this reaction can actually provide great buying opportunities for investors in the EMD universe.

Differentiating between local and hard currency debt

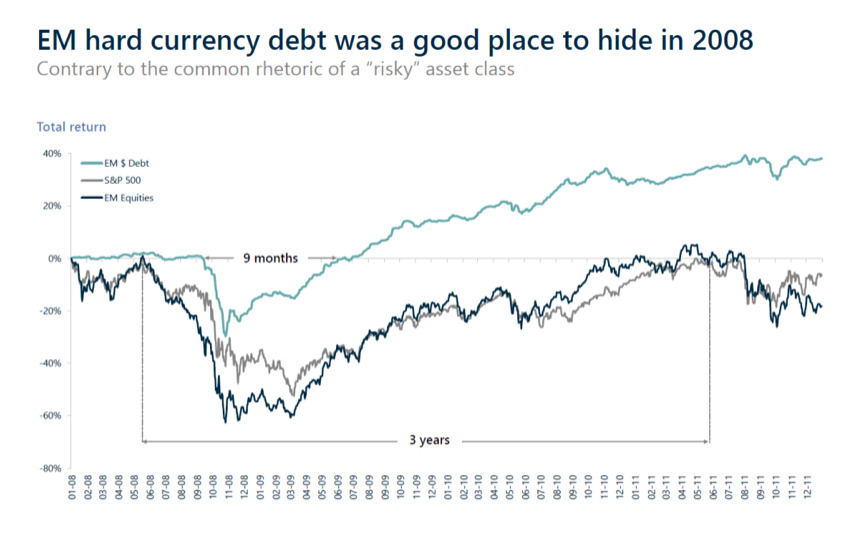

When considering the impact that a global slowdown might have on emerging markets (EM), Alejandro thinks it’s important to differentiate between two groups: local currency EM debt and EM equities; and hard currency EM debt. While it’s true that historically local currency EMD and EM equities have underperformed during downturns, the performance of hard currency EMD has actually been relatively consistent throughout the cycle. Looking at past data, recovery in hard currency EMD has been much quicker and stronger following global shocks; it’s about being positioned for those shocks.

During the last major financial crisis in 2008, it took only nine months for hard currency EMD to recover its lost value, compared to three years for cyclical EM assets. Looking back even further to when EM indices were launched in 1994 – a period that has seen boom/bust conditions in commodities, surging inflation and debt restructuring from certain countries – hard currency EMD has generated similar returns to the S&P 500 Index, but with half the volatility.

Why is this? The answer is that the emerging market universe is not homogenous, and it should not be treated as such: it is made up of 83 countries, each at different points in the economic cycle. Moreover, with a credit spectrum spanning AAA to CCC and bond maturities ranging from 0 to 100 years, active managers have the tools to build robust portfolios to mitigate risk and take advantage of opportunities.

Mitigating volatility

The first line of defence for mitigating volatility is differentiation in portfolio construction. Not all economies move in tandem and so depending on the point in the cycle, Alejandro positions the portfolio accordingly. As a strong believer in diversification, he keeps individual positions modest in size. There are enough corporate and sovereign names in the EM universe that he is able to reflect trends while still constructing very diversified portfolios. Hard currency corporate bonds, in particular, are not only the fastest growing asset class within EM, but they have also delivered the best risk-adjusted returns.

Alejandro uses credit default swaps to help manage volatility, especially for short-term shocks since it means he doesn’t have to sell the underlying bond holdings. For example, in 2019 he has employed CDS to manage the volatility in Russia, Turkey and Argentina. He can also use cash to take advantage of volatility: he doesn’t want to be a forced seller and cash means being able to ‘keep powder dry’ to buy when opportunities arise.

Seeking the best opportunities

With around $11tn of negative yielding debt globally, Alejandro believes emerging market debt will remain particularly attractive on a total return basis, as investors will look for opportunities outside of developed markets to generate returns. In his view, the current market environment makes it particularly important to focus on seeking out hard currency bonds issued by corporates and governments with the strongest fundamentals, which should be ready for the next cycle. For Alejandro, country differentiation and an agile investment style is key to finding the best risk-adjusted returns within emerging markets.