By Aaron Grehan, Deputy Head of Emerging Market Debt and Portfolio Manager, EM Hard Currency, Aviva Investrors

After one of the most volatile periods on record, hard currency emerging market debt is once again drawing investor interest, thanks to attractive yields and its diversification potential. But while markets recovered quickly from the volatility, investors should remain cautious for the challenges ahead.

COVID-19 brought about a supply and demand shock globally, but many emerging market countries suffered more than their developed counterparts. In addition to the pandemic, some emerging economies were also hard hit by external macro trends, particularly the oil-price war between Russia and Saudi Arabia in the spring of 2020 and continued tension in US-China trade relations.

Investors initially panicked, with about US$103 billion in non-resident capital flowing out of developing economies in the first quarter, according to data from the Institute of International Finance. Both equity and bond portfolio outflows “exceeded the worst points” of the 2008 global financial crisis, the 2013 ‘taper tantrum’ and the 2015-2016 China market turbulence.1 The premium investors demanded to own hard currency emerging market debt (EMD) over US Treasuries more than doubled from about 270 basis points (bps) in the fourth quarter of 2019 to 662bps on March 23 – a move that was astonishing not only for its scale but also its speed. Liquidity dried up, followed by heavy capital outflows.

However, thanks to unprecedented support in recent months from global central banks and multilateral agencies such as the International Monetary Fund (IMF), yields – particularly in investment grade hard currency debt – have returned to pre-crisis levels….”

This is a slight reversal from 2019, when investors sought the higher yields provided by countries of lower credit quality. So far this year, demand for debt issued by lower-rated EMD issuers has not recovered to the same extent due to the greater vulnerabilities that exist in those countries; spreads within the high-yield part of EMD market still remain about 240bps higher than pre-crisis levels, as of August 31. The market dislocation could provide more favourable return opportunities in this part of the market on a selective basis.

There are some indications the current rally in hard currency emerging market sovereign debt may have room to run. But given this is not a homogenous asset class, how do investors assess the relative resilience of EMD issuers? This article looks at a series of factors that are useful in gauging the strength of emerging markets, including debt sustainability, monetary and fiscal policy, access to liquidity and their record on environmental, social and governance (ESG) issues.

Bifurcating world

The EMD universe was not created equal. In the aftermath of the COVID-19 outbreak, that gap has widened further, particularly between investment-grade and high-yield countries. Some investment-grade sovereign issuers, including China, may have more capacity for fiscal and monetary intervention during crises than others and are therefore seen as safer. And within high-yielding countries, divergence is also increasing.

Unlike developed market fixed income, in which investment-grade and high-yield bonds form two distinctly defined markets, EMD combines both.

The blended nature of the EMD universe increases our flexibility to allocate between high yield and investment grade, and switch from attack to defence…”

says Aaron Grehan, deputy head of emerging market debt and hard currency portfolio manager at Aviva Investors.

However, it can also make asset allocation decisions more challenging, especially when the investment environment is fast-changing and uncertain. Reacting effectively to this environment requires a strong understanding of bottom up and top down fundamentals. “Ultimately, it’s about better utilisation of risks and return characteristics to manage volatility and smooth returns over time,” adds Grehan.

As a starting point, looking at how strong countries and companies were going into the current crisis – and their subsequent responses to the macro threats – may offer investors useful insight into their likely resilience in future, says Carmen Altenkirch, emerging market sovereign analyst at Aviva Investors.

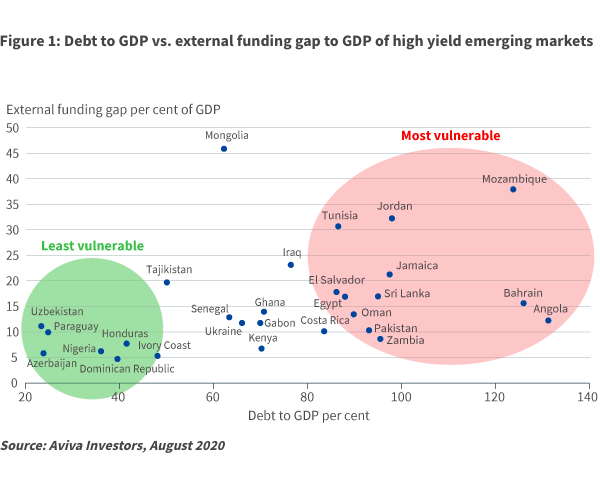

Two important measures are solvency and liquidity. Here, the gap between investment-grade and high-yield countries – already evident before the crisis – has widened further. Importantly for investors looking for opportunities to generate strong and consistent returns, divergence between high-yield nations has also increased (see Figure 1).

Relative to investment-grade emerging markets, high-yield emerging nations tend to have less firepower, such as unconventional monetary policy tools like quantitative easing, to stimulate their economies. Second, they usually have larger budget deficits and a higher cost of debt. Third, many of these countries are structurally weaker. Therefore, greater concerns have emerged around debt sustainability at a time when nations may be required to borrow more to support economies devastated by the pandemic.

Divergence is also widening among high-yield countries, which may be due to factors including how nations cope with the pandemic; impact of oil prices; reliance on tourism; level of exports of non-essential goods; and dependency on remittances. The latter surpassed foreign direct investment as the biggest inflow of foreign capital to emerging markets in 2019,2 but has fallen sharply this year as high unemployment among overseas workers left many unable to send money home.

“Knowing what is happening on the ground, between and within countries, allows you to see more clearly where the real risks are, enabling you to look beyond historical biases and make a more forward-looking assessment. This is particularly important in these uncertain times….”

IMF and debt relief

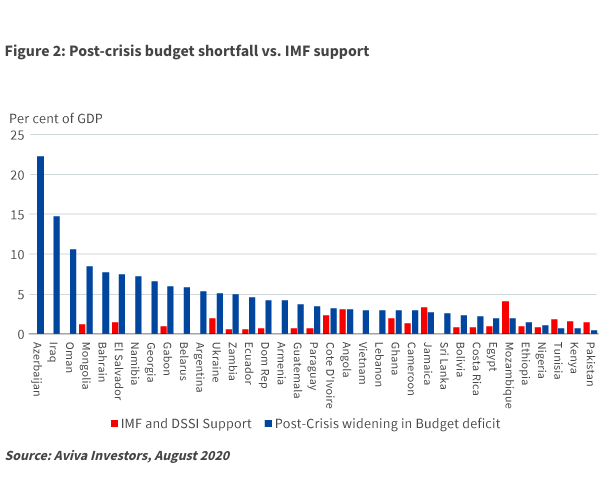

The IMF projects the overall fiscal deficit of 40 emerging market countries, including China, will increase by about five percentage points of gross domestic product in 2020, from 4.9 per cent in 2019.3 There have been at least 122 rating and outlook downgrades in EMD since March, according to Bank of America.4

Many issuers are facing “an unfolding global recession in a much more vulnerable position than when the 2009 crisis hit”, according to the IMF. And, as the crisis threatens to overwhelm nations’ ability to respond, the IMF and World Bank have provided crucial liquidity to prevent a spate of defaults (see Figure 2). In March, the IMF warned at least US$2.5 trillion in external financing would be needed to support developing nations.

“We have over a hundred countries that have come to the IMF. That’s more than half of the membership. That has never happened before,” said Gita Gopinath, chief economist at the IMF, at a Council on Foreign Relations event in May.5 “A second thing that’s unique about this crisis is that the demand now is for rapid financing. So it is not the traditional IMF program which has a lengthy discussion and a long period of financing and conditionalities.”

How the IMF chooses to apply financing rules during the health crisis will have significant consequences for investors, according to Altenkirch.

“The extent to which countries are able to continue to finance themselves easily and cheaply is one measure of how resilient they are,” she says. “If they struggle, will there be continued multilateral support coming from the IMF and the World Bank? Once the peak of crisis has passed, how willing are those countries to implement the necessary fiscal policy adjustments to regain their economic footing? That’s the key question.

Along with adequate policy support, a sustained market recovery will depend on economic growth, though that is increasingly difficult to forecast.

There is a lot of optimism at the moment. If that is justified and confirmed by data, risk assets will perform well, and EMD should perform strongly within that….”

“If we go the other way and start to see a worsening of the health crisis, pessimism will set in and we’ll experience deteriorating sentiment.” Grehan says.

Managing uncertainty

This means investors need to strike a balance between positioning for growth and preparing for worsening conditions. The high degree of uncertainty on multiple fronts makes that task more difficult, requiring an intricate understanding of risks within countries.

“Investors couldn’t have been expected to predict the pandemic – not many saw it coming. But they should have been able to determine what the impact would be if they understood the fundamentals and the risk inherent within the EMD investment universe,” says Grehan.

Turkey, which has experienced structural problems in its economy for years, highlights how policy missteps can leave a country vulnerable during a crisis. In the first quarter, it embarked on a dangerous mission to defend the lira, burning through at least US$17 billion of currency reserves in the process.6 Though its bond yields fell, reducing borrowing costs, this was accomplished at the expense of longer-term credit fundamentals.

“The outlook was perhaps more negative than conventional metrics may suggest,” says Grehan.

Conditions deteriorated further with the outbreak of COVID-19. Revenues dropped, partly due to a disruption in exports, which account for about 30 per cent of Turkey’s GDP, and a severe reduction in tourism, which usually contributes about 12 per cent.7 While the unemployment rate has been kept relatively stable at around 13 per cent as of August 31, it would be higher if not for a temporary ban on lay-offs and those on unpaid leave not being included in the official figures8.

Looking at the overall picture, Turkey’s government has been left with little room for manoeuvre due to the earlier efforts to defend its currency.

Emerging economies tend to be more impacted by factors outside their control than developed ones, and the negative effects of policy decisions can be magnified….”

The US Federal Reserve, for example, has much more room to conduct quantitative easing and lower interest rates to support the domestic economy than Turkey’s central bank.

That said, many emerging markets are beginning to follow in the Fed’s footsteps by launching QE programmes of their own. Similar to the impact of central bank loosening on developed economies, such policy tools could provide near-term support for EMD. Longer term, however, this could bring unforeseen negative consequences.

“What makes this more difficult is that the scale is much bigger and wider than previous crises,” Altenkirch says. “How countries choose to respond is potentially more unpredictable. You need to be ready to act quickly.”

Don’t ignore the social factor

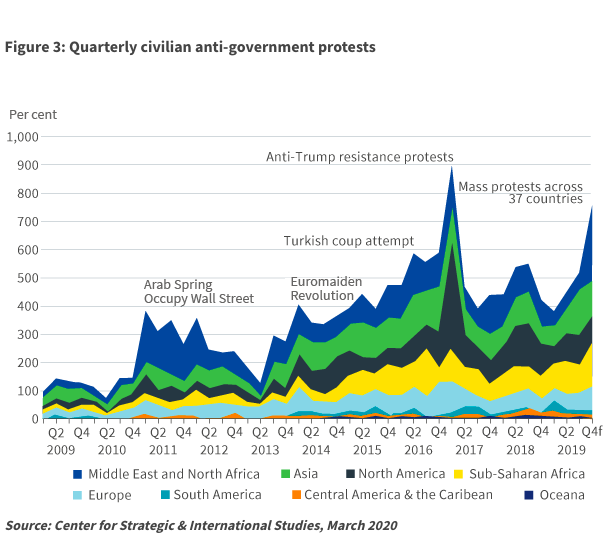

Another important element in helping investors to gauge resilience in EMD is the issuer’s ESG credentials. Governance has long been a key consideration and environmental factors including climate risks are playing a more important role. The social aspect, however, has generally lagged – until now. COVID-19 has made it essential for investors to analyse the extent to which nations and companies protect individuals and communities.

Social unrest, for example, can heighten investment risk. In the past ten years, there has been a steady increase in mass protests – a trend that appears to be on the rise across the world (see Figure 3).

Episodes of unrest have perhaps been most notable in the US and Hong Kong this year, but they have picked up throughout the world, most recently in Belarus. Since May, hundreds of thousands have taken to the streets to call for the removal from office of President Alexander Lukashenko after disputed election results that brought into question his political legitimacy, economic mismanagement and mishandling of the COVID-19 crisis.

Another case in point is Chile, a long-time favourite of emerging market investors for its relatively sound fiscal and monetary management in a region not known for it. However, prolonged social unrest erupted in October 2019 with dramatic implications for sovereign bond returns. The income gap, although decreasing, is stubbornly high with the share of GDP earned by billionaires the highest of any nation in the world, excluding tax havens.9

The triggers for protests may be different, but the underlying drivers tend to share common themes. In Chile, the drivers were deep-seated and intertwined, centred on inequality, inequity and instability….”

says Tom Dillon, macro ESG analyst at Aviva Investors. “This is accompanied by a strong sense of unfairness – worsened by the unfulfilled aspirations of groups including well-educated millennials who have relatively fewer job opportunities to earn a stable income, Dillon continues.

For example, a third of the labour force work in the informal sector are self-employed. Furthermore, about a third of those formally employed are on short-term contracts averaging ten months, interspersed with long periods of unemployment. The sporadic nature of employment has also exacerbated the precarious financial position of Chile’s pension system, once hailed by institutions such as the World Bank as a cornerstone of the country’s economic strength. In 2019, it became a central issue in the protest movement.

The economy suffered and the peso dropped to a record low, costing the central bank as much as US$20 billion in spot and swap operations to support the currency. Inflation expectations rose, so interest rates held steady even though economic activity had slowed. Meanwhile, the government responded to the protests by promising a national referendum on whether to rewrite the constitution, establishing a higher guaranteed minimum wage and enacting additional fiscal spending, including plans to boost pensions and improve healthcare. Dillon concludes;

“Even if civil unrest is short-lived, the policy responses to it won’t be…”

Focusing on resilience

Risk-return characteristics can change rapidly in EMD, so preparing portfolios for different scenarios is key to mitigating volatility. Prior to COVID-19, for example, there had been signs that spreads for several countries were not adequately compensating investors for the risk, especially in the investment-grade universe.

“Growth had been slowing and idiosyncratic challenges, particularly in single-B securities, were creating structural issues in a number of countries,” Grehan says. “At that time, putting a lot of scrutiny on specific countries within the portfolio and shifting towards higher quality assets helped mitigate volatility when conditions deteriorated as COVID-19 spread globally.”

One way of protecting an EMD portfolio is to increase exposure to investment-grade securities. However, within high yield, some countries will be better placed to weather the crisis. For example, low-debt countries with lower external financing requirements, such as Ivory Coast, Paraguay and Dominican Republic, may prove more resilient, Altenkirch says. Countries where risks may be mispriced, such as Pakistan, may also have potential. In the latter case, IMF support, economic reform efforts and interest rates of seven per cent as of June 2020 may provide attractive opportunities.

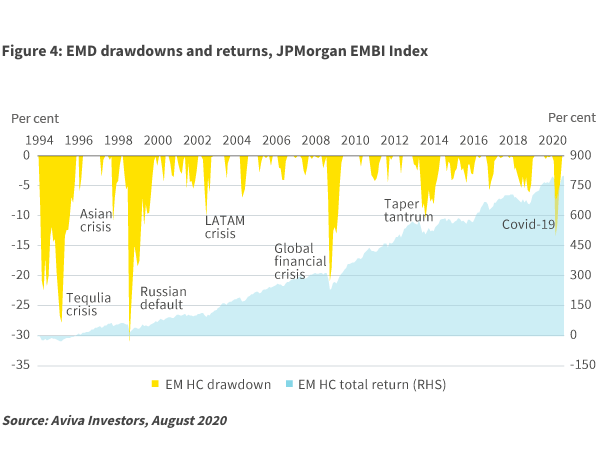

Significant EMD drawdowns of more than ten per cent have historically been followed by periods of strong performance (see Figure 4). The average 12-month return following a significant drawdown is about 30 per cent, according to analysis of the EMBI Global index by Aviva Investors.10 In addition, valuations look attractive at a time when large swathes of developed-market government and corporate bonds carry negative yields.

“The global policy outlook is positive, more so now than ever before,” Grehan says. “Given the actions taken by the Fed earlier this year, followed by the European Central Bank and other developed market central banks, and then by emerging market central banks in the form of lower interest rates and quantitative easing, the policy anchor looks to be strong.”

Previous crises have also encouraged better debt management among some emerging markets, including the establishment of larger reserves, stronger financial frameworks and more stable fiscal processes. For example, some of the worst-hit countries by the 1997-1998 Asian financial crisis, including South Korea, Indonesia and Thailand, made huge strides in shoring up their finances and domestic capital markets. Further efforts to mitigate external shocks were implemented following the 2008-2009 financial crisis and the 2013 ‘taper tantrum’. The current crisis, too, may result in improved credit quality among certain EMD issuers over the long term.

Traditionally, an upswing in EMD sentiment tends to attract investors targeting tactical opportunities, only to flee when turbulence hits. Consistently timing the market, though, can be difficult and costly if, as in March and April, illiquidity takes hold. A more sustainable option may be to adopt a structural allocation to EMD, based on a dynamic investment process favouring resilience, to realise attractive returns while mitigating higher volatility.

Market surprises such as COVID-19 may be inevitable, but like the body’s ability to fight the virus, an EMD portfolio that is strong going into the crisis will stand a better chance of being more resistant to the next downturn.

References

- ‘Macro notes: 2020 capital flows outlook for emerging markets’, Institute of International Finance, April 8, 2020

- Federica Cocco, Jonathan Wheatley, Jane Pong, David Blood and Ændrew Rininsland, ‘Remittances: the hidden engine of globalisation’, Financial Times, August 28, 2019

- M. Ayhan Kose, Franziska Ohnsorge, Peter Nagle, and Naotaka Sugawara, ‘Caught by a cresting wave’, International Monetary Fund, Finance & Development, June 2020, Vol 57, Number 2

- Megan Greene, ‘Investors are too complacent about emerging market risks’, Financial Times, July 2, 2020

- ‘The IMF and COVID-19: How to Relieve Emerging Economies,’ The Council on Foreign Relations event, May 7, 2020

- ‘Fitch Revises Outlook on Turkey to Negative; Affirms at BB-‘, Fitch Ratings, August 21, 2020

- Michaël Tanchum, ‘Can Turkey cope with COVID-19?’, The Turkey Analyst, April 13, 2020

- Daren Butler, ‘Turkish bank on layoffs keeps lid on jobless but labour participation languishes’, Reuters, August 10, 2020

- Branko Milanovic, ‘Chile: The poster boy of neoliberalism who fell from grace,’ October 26, 2019

- Barney Goodchild, ‘COVID-19 and a brief history of emerging market debt drawdowns’, Aviva Investors, April 2, 2020