By Mark R. Kielsel, Anna Dragesic and Mohit Mittal – PIMCO

As we shape our equity market expectations for 2021 we assume continued economic recovery supported by fiscal and monetary policy. More critical, we base our forecasts on the arrival of an efficient Covid vaccination that allows “normal life” by the end of 2021. We forecast 25-30% EPS recovery for most markets and “lower for longer” interest rates (US 10y 1.0% by 2021 yearend). As such, the constellation of TINA, FOMO and rebounding economic activity should support further market upside for equities.

Credit markets experienced a roller coaster ride in 2020. Credit spreads initially widened as the emerging COVID-19 pandemic weakened risk sentiment and liquidity, and the global economy was temporarily shut down. But rapid, massive stimulus from central banks and fiscal authorities led to a quick recovery.

Although recent successes in developing and deploying coronavirus vaccines have encouraged investors to look past near-term economic weakness, the pandemic has amplified long-term disruptors, increasing the importance of credit selection and alpha generation.

Disruptive forces still at play

Fiscal and monetary support have shored up liquidity and staved off widespread defaults but will not cure solvency issues from over-levered balance sheets.

Early in the pandemic, companies went into self-preservation mode, supporting free cash flow by cutting capital spending and increasing liquidity. However, in our view, a return to pre-pandemic fundamentals for the most-affected companies could take years.

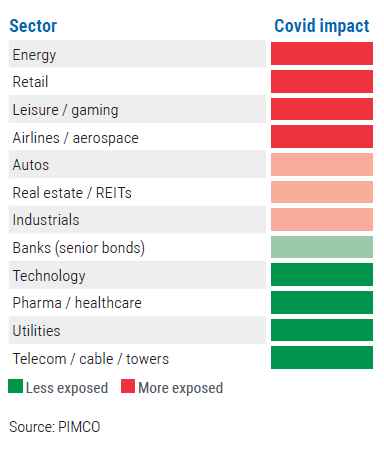

As shown in Figure 1, the economic impact of the pandemic has varied widely.

As you can see, certain sectors have been relatively insulated and, in some cases, have even benefited from increased demand; examples include healthcare and technology. Conversely, the travel and entertainment industries have seen their earnings severely affected, which has increased insolvency risk.

Although these sectors present risks, they also offer unique opportunities through careful credit research. Analyzing balance sheets and income statements over a wide range of scenarios becomes extremely important in this environment, as does structuring bonds so that bond holders have adequate covenant and collateral protections. We believe it’s important for investors to focus on secured structures with strong collateral and covenants when investing in these affected sectors in order to mitigate downside risks.

So, where do we go from here? While one likely scenario is a return toward “normal” in a post-pandemic world, changes in consumer and corporate behavior cannot be ruled out – the magnitude and extent of which are highly uncertain. We believe these changes will create winners and losers. Winners will include companies that can adapt and prevent their business models from getting disrupted. Losers will include businesses that cannot successfully adapt to changing preferences in a post-pandemic world. Differentiating between the winners and losers will require careful credit and scenario analysis.

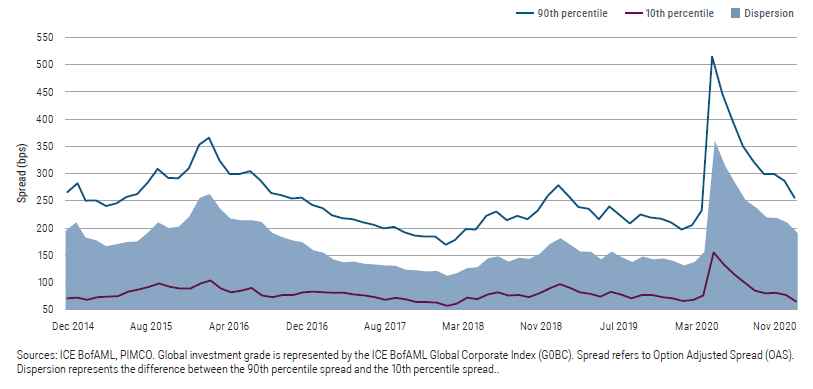

Credit dispersion remains elevated

Although credit spreads have largely narrowed in the past three quarters, we still see plenty of spread dispersion, which creates opportunities for active managers like PIMCO. For example, investment grade credit spreads are tighter than their long-run averages, but below the surface, dispersion is reminiscent of the 2016 period when the collapse in oil prices led to a significant widening in credit spreads. Despite positive vaccine developments, there is still a meaningful uncertainty premium in credit spreads – particularly in pandemic-affected market segments like transportation, energy, lodging, and entertainment.

The high yield market is similar in that issuers most exposed to pandemic-related restrictions are trading meaningfully wide of pre-pandemic levels. The high yield market has seen a big change in its composition after the massive influx of so-called fallen angel bonds – those that have seen their credit ratings downgraded from investment grade to high yield. Fallen angels have added more BBs, larger capital structures, and longer maturities to the universe, which stands in stark contrast to the smaller and shorter maturities of the CCC bond market.

Downgrades and defaults have likely peaked

This past year also saw an uptick in downgrades and defaults. Credit rating agencies were quick to act in March and April, but the percentage of bonds on negative outlook and negative watch has since decreased, and November saw more rising stars (bonds that have seen their credit ratings upgraded from high yield to investment grade) than fallen angels.

Although a number of household names defaulted, including several high-profile retailers, as well as a longer tail of smaller energy issuers, these business models were facing headwinds even before the coronavirus. And while energy issuers will likely account for the majority of high yield defaults in the year ahead, other sectors will also come under pressure.

Overall, default rates should be lower in Europe than in the U.S. given the higher quality of the European high yield market and a significantly lower concentration of energy companies. In addition, the absence of an equivalent to the U.S. Chapter 11 bankruptcy process makes in-court restructuring in Europe a measure of last resort, as opposed to a strategic one. Still, market indicators increasingly point to the end of the default phase and the beginning of the recovery phase.

Of course, in a bear case where vaccines prove to be less effective than expected, default risk will increase. Also, default risk remains high for smaller companies that received less direct fiscal support, those with limited collateral to pledge in exchange for liquidity, and firms facing secular headwinds even before the onset of COVID-19.

Opportunities in 2021

With roughly $17 trillion in fixed income bonds trading at negative yields, we expect demand for high quality sources of income to remain robust in 2021.1 We anticipate that global monetary policy will remain accommodative, which provides an additional source of support to credit markets. Strong global fiscal support will likely continue to provide a bridge to the credit markets until vaccines are more widely distributed, which could help facilitate the recovery of corporate fundamentals. This constructive backdrop should provide solid support for credit markets in 2021, even as some valuations may not offer as much room to rally. As active managers, we are excited about the bottom-up opportunities we see amid an uneven recovery.

Currently, we see several key opportunities in the public credit markets:

Post-pandemic recovery trades

Within the public credit markets, we favor select “recovery trades,” which involve firms we believe are positioned to benefit from economic reopening. Examples include airlines, hospitality, and REITs. Many such companies have raised enough capital to bridge to a post-vaccine recovery, and business functions have been optimized to operate in a post-pandemic world. As vaccines are deployed globally, many companies in these sectors should see earnings growth that helps them begin to recover and de-lever. However, vaccine deployment and economic reopening will not resuscitate sectors facing longer-term secular pressures. For example, we continue to be cautious about retail companies with limited online presence, long-dated auto bonds alongside the move toward autonomous capabilities, and traditional energy companies given the growth of renewable power generation and ongoing environmental, social, and governance (ESG) concerns.

Financials

We also see opportunities in financials given the strong cyclical recovery expected in 2021 and Democrats’ success in the Georgia U.S. Senate runoffs. Combined, these developments could stimulate fiscal spending, which should stabilize asset quality metrics and support net interest margins (the difference between what banks pay out in interest and what they receive) from a steeper yield curve. Unlike their substantial role in the global financial crisis, banks are not at the center of the current crisis but could be part of the solution.

We are focused on industry leaders, and we are willing to go down in the capital structure in order to invest in higher-yielding preferred securities. In Europe, we favor subordinated bank debt (AT1s) with a focus on U.K. banks, as we expect yield compression following the removal of Brexit uncertainty. We also favor select continental European banks with strong balance sheets and attractive valuations relative to generic high yield credit.

Housing

Additionally, the pandemic continues to benefit housing demand as a result of migration to single-family homes, low interest rates, and work-from-home arrangements. In turn, increased investment in home improvement projects has allowed building product manufacturers to raise prices. We find value in building materials companies with leading market share, residential REITS, and non-agency mortgages.

Select emerging market sovereign and corporate exposure

We are also increasingly focused on select opportunities within emerging markets. There is a high level of value dispersion within emerging markets, and so our focus has been on liquid sovereigns and quasi sovereigns that we believe are distanced from left tail events. Asian credit is also compelling given higher yields and strong growth prospects relative to developed markets. We are specifically focused on corporate sectors in Asia with attractive relative value, such as technology, property, diversified financials, and utilities but remain wary of China’s local government financing vehicles.

In addition to opportunities in global public credit markets, we also see value in private and less-liquid credit. While central banks have used tools that supported more traditional areas of the market, this liquidity hasn’t yet found its way into the private market, so private credit valuations remain attractive, in our view. The pandemic has dramatically altered credit provisioning across private lending markets. Complacency and borrower-friendly structures have been replaced by uncertainty and lender-friendly terms. In addition, a complex regulatory backdrop is creating opportunities to fill capital gaps for private lenders. Key areas of focus include secondary opportunities in residential and consumer-related credit, as well as commercial opportunities across small business, aviation, litigation finance, and other receivables.

Finding investment returns given today’s backdrop will require extensive fundamental research capabilities. We believe investors who utilize active managers with deep resources, a diversified credit platform spanning public and private credit, and extensive quantitative expertise will ultimately be rewarded.