By Jonathan Davies, Client Portfolio Manager, EM Debt at PineBridge Investments

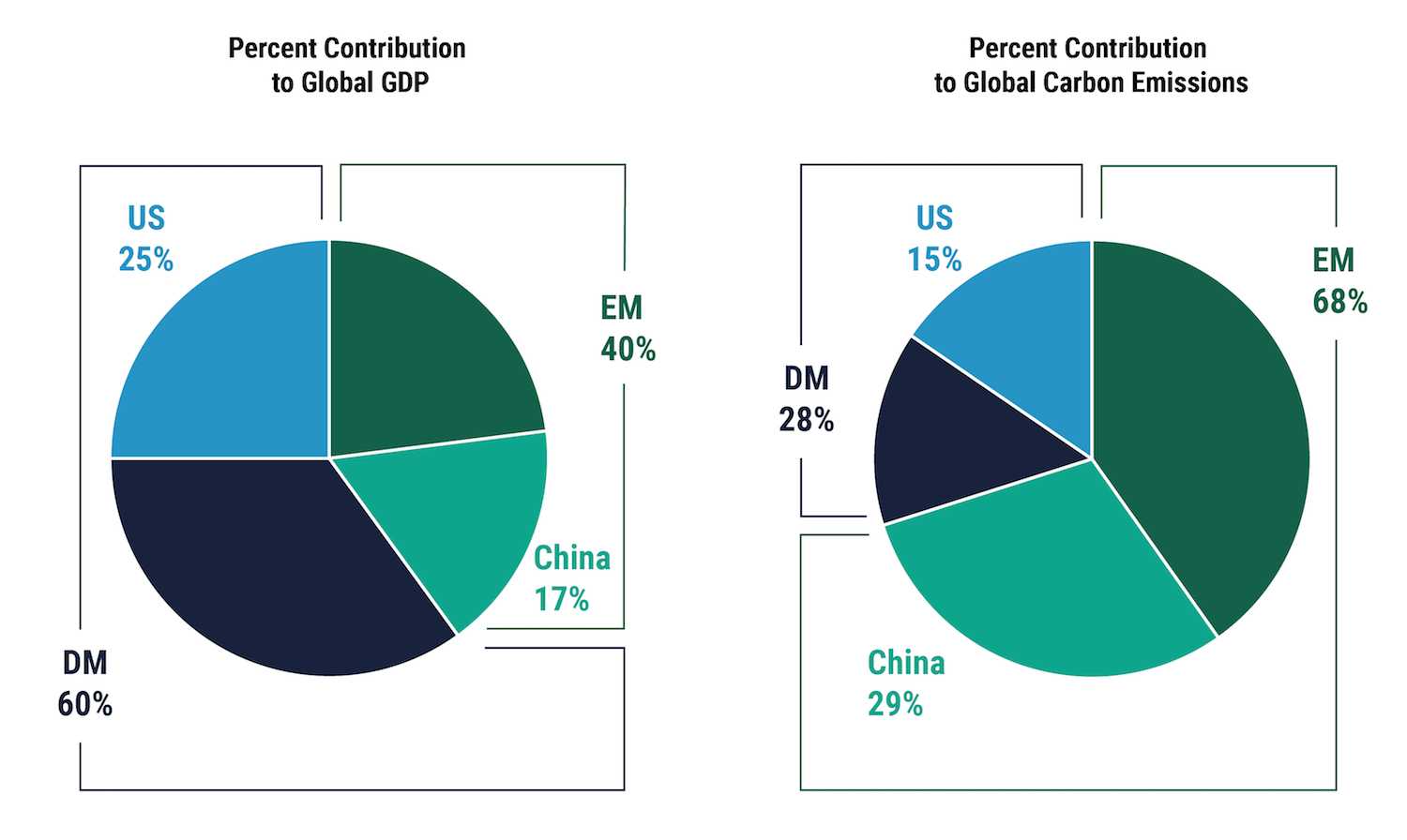

Emerging market (EM) investors will take on an important role in the global reduction of carbon emissions. EMs represent 40% of the global economy¹ and are responsible for more than 60% of global carbon emissions. China, of course, is the key contributor to the role of emerging markets within both the global economy and global carbon emissions.² Just as China needs to invest in cleaner sources of electricity and greener industrial production, EMs globally have similar investment needs. Broadly speaking, EMs are dependent on foreign direct investment and global capital markets, so initiatives like the G7’s commitment to halt funding of coal-fired power stations can make a meaningful impact.

Within capital markets, EM corporate issuers experience a substantial difference in cost of capital between those rated higher and lower on environmental, social, and governance (ESG) issues, which means asset owners and asset managers can make a material impact on the incentives for EM issuers to invest in carbon-reducing technologies. Recently, we have seen a rise in EM corporate issuers taking advantage of demand for green investment and the subsequent lower cost of capital to issue sustainability-linked bonds, which have coupon step-ups directly linked to decarbonization targets during the bond’s term.

Emerging Markets Represent 40% of Global GDP and More Than 60% of Global Carbon Emissions

ESG integration helps spot opportunities for alpha

Many investors believe EM economies are typically commodity exporters that will be challenged by commitments to reduce carbon emissions. First, it’s important to understand that while a number of net commodity-exporting economies are within emerging markets, so are just as many net commodity-importers. Second, it’s also important to understand that while decarbonization will cause demand for fossil fuels to drop, a number of other commodities play an integral role in the green technologies that will foster decarbonization and therefore will experience structural increases in demand.

At PineBridge, we have a history of focusing on alpha generation through bottom-up credit analysis and security selection. And we find most opportunities for decarbonization-related alpha will come within those sectors that make significant contributions to global carbon emissions, but with potential to adapt to a carbon-neutral reality that will generate outperformance of early adopters.

The goal is environmental and financial sustainability

The decarbonization of our planet is vital to its sustainability, and the coordinated commitment of governments, financiers, and corporate entities toward that goal is essential to its success. In our role as asset managers, we have a responsibility to contribute to environmental sustainability efforts and a responsibility to ensure that our clients’ portfolios are positioned for financial sustainability as well.

With so much of this story yet to be written, we have identified three must-have attributes within our ESG framework that will enable our investments to both promote decarbonization and to profit from it. First, we find it essential to prioritize an integrated, forward-looking ESG trend within our analysis of ESG risk. Second, we must be prepared to look to the future and not necessarily exclude exposure to carbon, but rather to include exposure to entities that are moving toward lower-carbon processes. Third, we must maintain an engagement framework to identify and encourage issuers to make investments in green technology – investments that will make their business models not only more sustainable, but also more profitable in the carbon-neutral world of the future.

For further information please see Decarbonizing the World: The Key Role of Asset Owners and Managers

Sources:

1 IMF and Bloomberg as of 31 March 2021

2 IMF and Bloomberg as of 31 December 2021

Disclosure

Investing involves risk, including possible loss of principal. The information presented herein is for illustrative purposes only and should not be considered reflective of any particular security, strategy, or investment product. PineBridge Investments is not soliciting or recommending any action based on information in this document. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author, may differ from the views or opinions expressed by other areas of PineBridge Investments, and are only for general informational purposes as of the date indicated. PineBridge Investments does not approve of or endorse any republication of this material.