By David van Bragt, Investment Solutions Consultant, Aegon Asset Management

Many institutional investors have been attracted in recent years by the potential for high yields on mortgage investments. Exposure to the mortgage market can be achieved in various ways. An interesting approach is used in Denmark: in this country, mortgage loans are coupled to mortgage bonds that have a very high rating and can be traded in a liquid secondary market. In this article, we compare these Danish mortgage bonds with direct investments in Dutch mortgage loans.

This analysis informs institutional investors about the distinguishing features of these markets in mortgage-related instruments.

The general characteristics of the Dutch and Danish mortgage market are quite similar: both markets are large, well developed and supported by households with (on average) a high net worth. The following distinction is particularly important, however:

- Dutch mortgages are direct loans. They are accessible via funds, special purpose vehicles (SPVs) or separate mandates. Investments are typically made via a pool of thousands of mortgages. The total size of the Dutch mortgage market is around €740 billion.

- Danish mortgage bonds are listed bond issues, whose notional and coupon reflect the notional and coupon of a pool of similar mortgages on a pass-through basis. They can be directly accessible via an investment in listed bonds, or via fund structures. The market for Danish mortgage bonds is one of the largest covered bond markets in the world (around €390 billion).

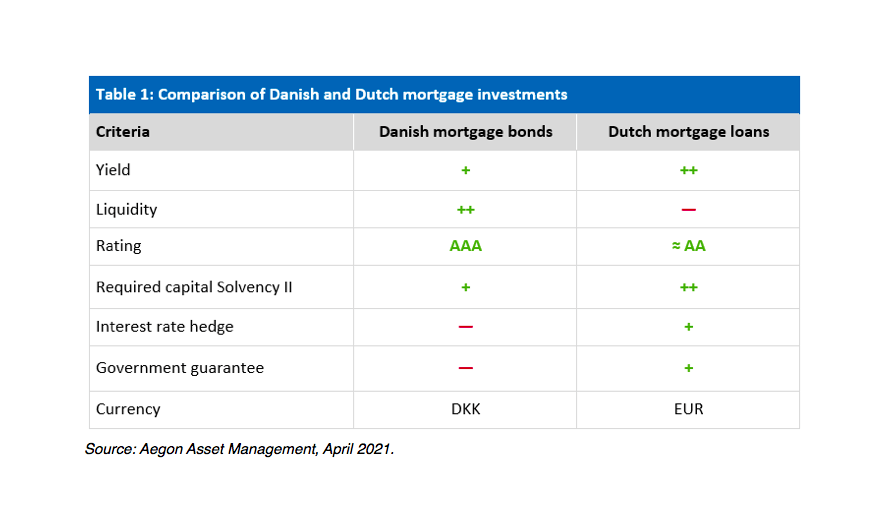

A global comparison of Danish and Dutch mortgage investments is showed in Table 1:

We discuss the different criteria in this table in more detail below.

Yield

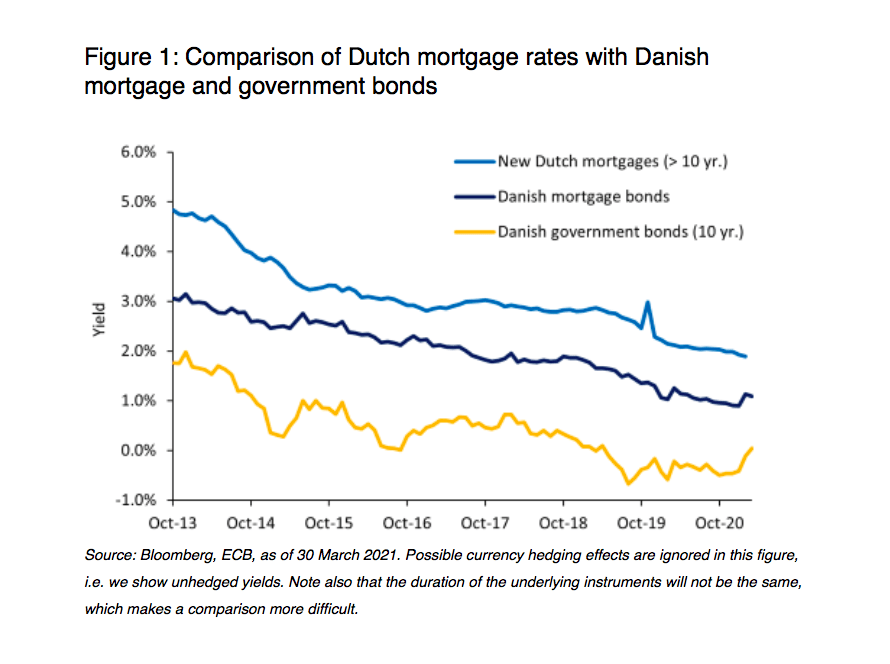

We give an impression of the yield on Danish mortgage bonds in the figure below. For mortgage bonds, we here show the yield from the Nykredits Realkreditindeks. As a comparison, we also show the yield on 10-year Danish government bonds and new Dutch mortgage loans (with a maturity over 10 years).

Note that Danish mortgage bonds typically offer a spread of around 1-2% over Danish government bonds, mainly as a compensation for the embedded options in these instruments. The rate on new (long-term) Dutch mortgages is typically circa 1.0% higher than for Danish mortgage bonds. This is mainly a compensation for the less liquid direct mortgage loans, compared to the liquid Danish mortgage bonds.

Figure 1: Comparison of Dutch mortgage rates with Danish mortgage and government bonds

Liquidity

Danish mortgage bonds have the advantage of being more liquid than Dutch mortgages. These financial instruments are bonds listed on an active secondary market (providing daily liquidity in practice).

Rating

Danish mortgage bonds are typically rated AAA. Dutch mortgage loans are unrated instruments. Pooled funds with a large number of Dutch mortgages typically have an internal rating of AA.

Required capital under Solvency II

Dutch mortgages and Danish mortgage bonds have a mitigating impact on the required capital for interest rate risk, with some added complexity in case of callable Danish mortgage bonds due to the embedded prepayment options (see the analysis in the next section). Danish mortgage bonds are treated as covered bonds under the standard model of Solvency II. The Solvency II capital charge for covered bond loans is depending on the rating and the (spread) duration in this case. Capital charges for covered bonds are lower than for corporate bonds for similar ratings and durations. For example, capital charges for AAA corporate bonds and AA covered bonds are the same. Danish mortgage bonds are typically rated AAA. If we assume that the (spread) duration is approximately 5, this leads to a capital charge for spread risk of around 3.5%. For example: Danish government bonds have a capital charge for spread risk of zero under Solvency II, whereas Danish corporate bonds with a rating of BBB and a duration of 5 would have a spread capital charge of around 12.5%. The capital charge for Danish mortgage bonds is thus at the lower end.

The capital charge for Dutch mortgages is typically calculated using the default risk module, instead of the spread module. Approximately, a capital charge of around 4-5% would apply for default risk, depending on the loan-to-value. However, as this default module has a low correlation with other modules (0.25), the overall capital charge for Dutch mortgages is very small under Solvency II. In fact, the added capital charge on the overall balance sheet level is approximately equivalent to adding an asset class with a spread risk charge of only 2%. Note that Danish mortgage bonds do not qualify for the default risk module (only residential mortgage loans can qualify for this module).

Capital charges for spread or default risk are thus low for Danish mortgage bonds and even lower (in equivalent terms) for Dutch mortgages under Solvency II.

Interest rate hedge

Dutch mortgages are less complex in terms of embedded options, in particular when considering the higher prepayment risk of Danish mortgages. Prepayment is possible without a penalty for Danish mortgages which are linked to callable mortgage bonds. This has an impact on the duration of these bonds. A non-callable bond typically has a relatively stable duration if interest rates change. Depending on the maturity of the bond, the duration will increase at lower interest rate levels.

A completely different picture emerges, however, for callable Danish mortgage bonds. In this case, the bond will be called (at par) with a higher probability at a lower interest rate level. This means that the duration of these loans will typically decrease (instead of increase) at lower interest rate levels. As a result, Danish mortgage bonds are less suited as an interest rate hedge instrument for investors with long-term liabilities. When the duration is needed (at low interest rate levels), the bonds can be called, which results in a deteriorating interest rate hedge.

Government guarantee

In the Netherlands, a large mortgage insurance structure is in place: the “Nationale Hypotheekgarantie” (NHG). The “Stichting Waarborgfonds Eigen Woningen” (WEW) is an entity that issues NHG mortgage loans. The WEW guarantees approximately €190 billion in mortgage loans and is fully guaranteed by the Dutch central government. Based on this, a Dutch NHG mortgage loan can be considered to be government-guaranteed. Note, however, that the NHG guarantee does not cover all losses. For example, for new mortgages with an NHG guarantee an own risk clause of 10% of the losses applies. In Denmark, mortgage insurance structures do not exist.

Currency risk

Danish mortgage bonds are mostly denominated in Danish kroner. For euro investors, the currency risk is limited when investing in Danish mortgage bonds because the Danish krone is pegged to the euro.

Conclusions

Based on our analysis, we conclude that Danish mortgage bonds may be an attractive alternative to Danish government bonds (higher yield, high liquidity, low capital charge). For investors who allocate part of their assets to illiquid categories, Dutch mortgages can offer an additional spread compared to Danish mortgage bonds. The Dutch mortgage product is also less complex in terms of embedded options, in particular with respect to prepayment risk which may manifest itself in case of decreasing interest rates.