The COVID-19 pandemic has accelerated digitalization and technological change in finance. It has boosted demand for digital services and alternative currencies, with factors such as multiple rounds of stimulus, accommodative monetary policy and excess liquidity contributing to record inflows into Bitcoin. The ongoing progress in digital technology has given rise to online start-ups without a banking background and the expansion of social media and digital platforms into credit and payments, bringing fintech into the mainstream.

“The market has fixated on the rally in Bitcoin, but the real economic and exciting action is in the new battle for digital supremacy between the banks and fintech,” said Joyce Chang, Chair of Global Research. “We expect to see intensifying competition and innovation with major IT capital expenditure (CapEx) forthcoming on both sides.”

Steven Alexopoulos, U.S. Mid- and Small-Cap Bank Analyst, believes that traditional regional banks could emerge as endgame winners in the digital age of banking. “Big Tech possesses the most potent digital platforms due to their access to customer data, but banks have an advantage from deposit franchise, risk management and regulation,” he noted.

Fintech in Asia leading the transformation

Transformation is occurring most rapidly in Asia, which continues to drive third-party (noncash) global growth in payments. In China, the COVID-19 lockdown induced wider acceptance and usage of mobile banking, while J.P. Morgan estimated the total addressable market for third-party payments in the ASEAN 6 countries (Indonesia, Thailand, Singapore, Malaysia, Philippines, and Vietnam) at $1.5 trn. “There is tremendous scope for growth as penetration is low at only 2%,” according to Harsh Wardhan Modi, Co-Head of Asia ex-Japan Bank Research.

Is Bitcoin here to stay as an alternative currency?

The rise in Bitcoin’s acceptance as an alternative currency is another phenomenon of the COVID-19 era. Demand for an unconventional and high-volatility hedge has been driven by rich equity and credit valuations; conventional hedges like developed-market bonds barely serve as insurance at current low yields. Concerns about cyberattacks, climate catastrophes and materially higher inflation also factor in, particularly with millennials, furthering demand for these unconventional financial channels.

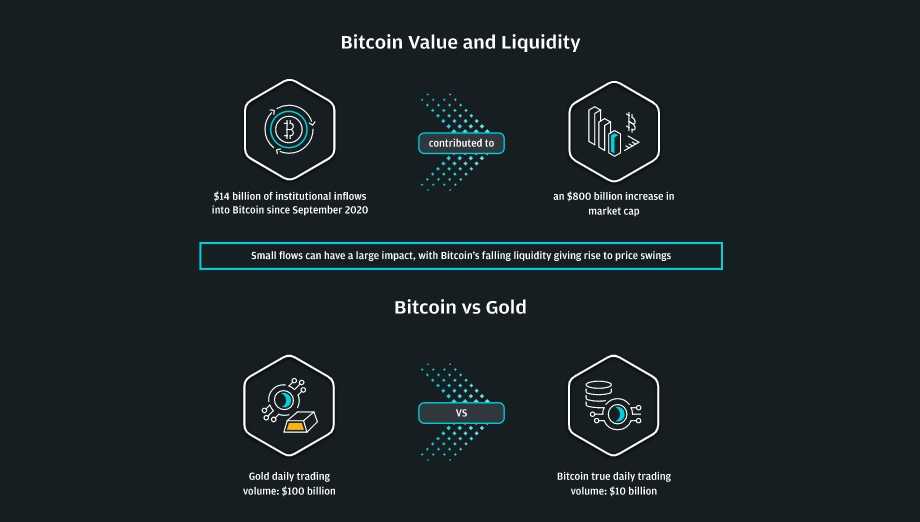

“Bitcoin has already surpassed gold in risk capital terms,” according to Nikolaos Panigirtzoglou, Senior Global Markets Strategist. “Current prices are well above our most recent estimates of fair value based on mining cost and risk capital equivalence with gold.” He observed that just $14 billion of institutional inflows into Bitcoin since September 2020 have contributed to an $800 billion increase in its market cap. Some of this can be explained by low market liquidity.

Panigirtzoglou estimated that, at $100 billion, the daily trading volume of gold in spot and futures is 10 times the true trading volume of Bitcoin. Mika Inkinen, Global Markets Strategist, added “We estimate the long-term theoretical Bitcoin price at $146,000 to match the total private sector investment in gold via ETFs or bars and coins.” Reaching this would likely be a multi-year process that would depend on far greater institutional Bitcoin ownership and on the volatility of bitcoin converging to that of gold, he said. So far the opposite is happening, with the volatility of bitcoin rising while the volatility of gold is falling. At the current bitcoin to gold volatility ratio of around four times (in terms of six-month volatilities), the fair value for bitcoin in risk capital (i.e. risk-adjusted) terms drops to around $37,000.

The diversification benefits remain questionable at current prices so far above production costs, while the mainstreaming of cryptocurrency ownership is raising correlations with cyclical assets. “Crypto assets continue to rank as the poorest hedge for major drawdowns in equities, particularly to fiat currencies like the dollar which they seek to displace” notes John Normand, Head of Cross-Asset Fundamental Strategy. “To the extent that Bitcoin remains an investment

Bitcoin’s Price: is it Built on Solid Foundations?

Recurring Bitcoin price surges beyond intrinsic value (estimated mining costs) are one reason to expect long-term mean reversion.

While on-screen liquidity in Bitcoin markets has continued to improve as acceptance has grown, Josh Younger, Head of US Interest Rate Derivatives Research, cautions that this has largely come from high-frequency traders who can quickly exit the market when volatility picks up. He highlights the tail risk to Bitcoin markets if there were to be a sudden loss of confidence in USDT, a Stablecoin issued by Tether Ltd; Bitcoin relies on this for 50-60% of trades. “Bitcoin is only as strong as the foundation and a sudden loss of confidence in USDT would likely generate a severe liquidity shock to Bitcoin markets, which could lose access to by far the largest pools of demand and liquidity,” Younger said.

Is blockchain technology moving into the mainstream?

While blockchain technology could not be considered mainstream yet, it is moving beyond experimental early stages. In 2020, J.P. Morgan launched Onyx, a new model for financial innovation that incorporates blockchain technology, becoming the first global bank to create a dedicated unit to develop and scale blockchain-based products. Onyx’s mission is to reimagine business and the ways it can be transformed, with the new infrastructure, networks and services enabled by distributed ledger technology.