By Hamlin Lovell, NordicInvestor

“In my opinion, Asian credit now offers one of the three most compelling environments I have seen over my thirty-year career. The other two were after the global financial crisis in 2008 and the Asian financial crisis in 1998” says Rob Petty, co-founder of Clearwater Capital Partners (“Clearwater”).

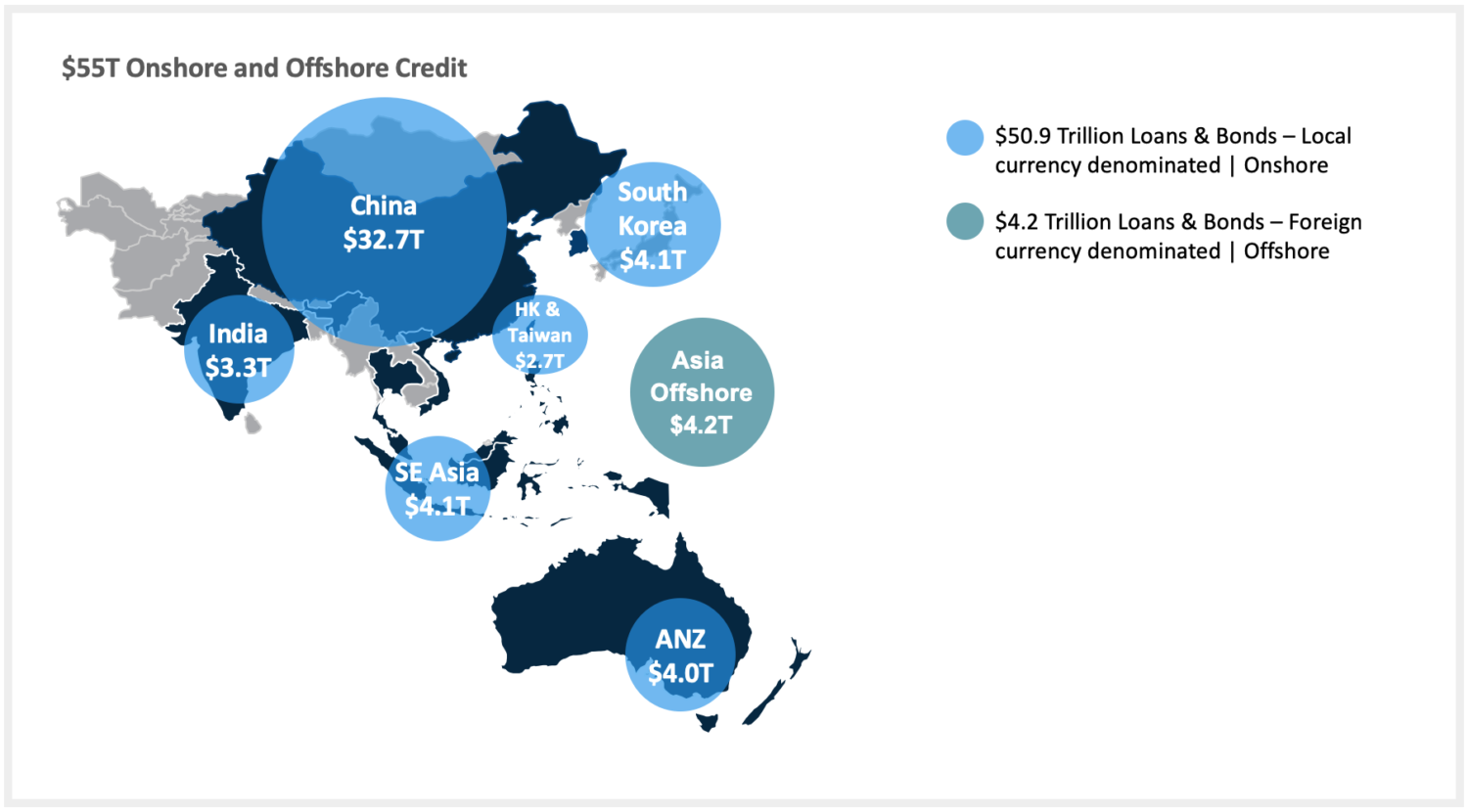

Based on Clearwater’s internal assessment, the offshore market for liquid, USD denominated Asian-ex Japan credit – loans and bonds – is currently valued at around USD 4.2 trillion and can now be paying as much as 300 to 500 basis points more than comparable names in US High Yield. “Yields are some of the highest we’ve seen, and stable, cash-generative returns should show lower volatility than equities in the uncertain year ahead” says Petty. Moreover, amid escalating concerns over ‘covenant-lite’ lending in the US, he argues that, “covenants are better in Asia, companies who borrow in offshore dollars are much better capitalized today than they used to be, and there is a 10 year history now that shows Asian High Yield has lower default rates and higher recovery rates than US High Yield”.

Meanwhile, in the illiquid space, private direct lending deals can reportedly yield as much as 15%, at the very top of the capital structure, in senior, secured deals, in Australia, South Korea, Hong Kong and Singapore. Funds are “the new banks” in Asia and Australasia, just as they are in the US and Europe, but yields can be much higher than the 8-10% typically seen in some North American private lending deals, while the legal environment in these countries is often just as creditor friendly as the US.

The proximate cause of the repricing – which has seen substantial performance drawdowns in Asian High Yield indices – is likely attributed to a confluence of factors, including the rising rate environment onshore in China, the US/China trade war, flight to safety in late 2018, and general concerns over a slowing global economy.

The longer term, multi-year driver for higher yields is that banks’ deleveraging reduces the supply of capital. Clearwater sources some deal-flow directly from banks and in other cases is replacing banks by originating its own deals. “Asia is in the second stages of addressing over-leveraged businesses and non-performing loans especially in Chinese manufacturing” says Petty. He does not doubt that overcapacity exists in core manufacturing businesses of steel, cement, shipping, and semiconductors but, at the same time, leading players in these industries can continue to profit – and need capital to sustain this growth.

Clearwater’s credit ecosystem

Clearwater is one of the most seasoned alternative asset managers in Asia and has just celebrated its 18th year, most recently as the Asia Credit arm of Fiera Capital. Over that period, it has invested over $7,3 billion in stressed, distressed, direct lending and special situations opportunities in Asian credit markets. Average holding periods have been around 2 years and exits can occur via sales, scheduled payments, liability management or early refinancing. The return profile from these types of idiosyncratic deals has historically been moderately or lowly correlated to publicly-traded equities and high yield debt instruments in the US, Asia and Europe.

“The vast majority of investments have performed and repaid, but in stressed, distressed and direct lending, the firm sometimes goes through workout processes. This is all part of the strategy, which might involve buying a distressed name at 40 cents on the dollar, with the expectation of recovering multiples of that, or buying a performing credit at 70 cents and realising principal and interest through scheduled or rescheduled payments. Sometimes there are debt for equity swaps, such as our investment in Suzlon convertible bonds which were restructured into roughly half debt and equity and have now been exited over time. We bought convertible debt in Suzlon, India’s biggest wind turbines supplier, at around 50 cents on the dollar, and working with the company, helped them with the restructuring which ultimately enabled us to double the money for our investors” says Petty.

Clearwater operates in the largest economies of Asia and has built direct lending operations across developed markets such as Australia and Korea where legal frameworks are well accepted. They have also found India and China to be strong documentary locations when they are writing original loans themselves. “If you write good documentation, you can enforce covenants and make recoveries, in markets such as India and China, where we have large scale direct lending operations. NPLs in China are more of a collections business than a restructuring business, and we own an NPL servicer in China” observes Petty.

He acknowledges that parts of Southeast Asia are still emerging markets, including in enforcement terms, hence country exposures are chosen carefully. Clearwater has historically done deals in countries such as Vietnam, Indonesia, the Philippines, Thailand and Malaysia, but currently finds that larger economies offer enough ample opportunities for the firm to be selective.

Petty, who is regularly invited to speak at Milken Institute events, stresses that “asset managers need a dedicated, focused ecosystem of infrastructure to avail of these opportunities. We have lawyers, underwriters and industry specialists so we can be analytical and responsive. We currently have a developed Asia team in Hong Kong; an office in Singapore; over 25 people on the ground in Chongqing, China; an office in South Korea; over 50 people in our JV platform Altico in Mumbai, India, and a network of strategic partners across multiple markets. We view ourselves as being one of the three key direct lending players in the region”.

Fiera Capital (Asia) has since August 2018 been the corporate umbrella for Clearwater Capital Partners Asian credit platform; with parent Fiera Capital Corporation in Montreal bringing CAD 143 billion of assets in traditional and alternative strategies to the table, as well as a listing on the Toronto Stock Exchange.

Potential further volatility

It is hard to call a trough in any market, and Petty is well aware that Asian credit could have another lurch down, perhaps if the US-China trade war escalates or if economic data disappoints. “We take a long-term view, and want to buy credit when people hate it” he says.

Petty’s forecast for China’s economy slowing down to below 6% growth is worse than consensus, but even under this scenario he expects plenty of fundamentally sound businesses can service and repay their debt. Meanwhile, Petty reckons India’s economy could advance as fast as 7.5%, and points out that even with some degree of slowdown, Asia could still be growing twice as fast as the developed rest of the world.

Petty also feels reasonably relaxed about the possibility of further declines in Australian property, which provides the collateral for some of Clearwater’s lending deals. Australian property is down 11% from the peak 1.5 years ago, but real estate in many major cities worldwide has also been on the decline. Clearwater’s exposure in Australia illustrates its relatively cautious approach: “we do not expect more than 15% further downside, and we are doing senior, secured property lending at 65% loan to value ratios. We are not involved in luxury, multi-million-dollar properties, but rather are in “real people housing” and those themed around Australian universities, which have robust demand from Asian parents sending their children to study there” he says.

“South Korea is another promising market for property development, as the construction giants that became over-leveraged have retreated, making space for mid-market players” he adds.

Overall, Petty sees a sufficient pipeline of compelling deal-flow to deploy substantial capital, creating an opportunity to target upwards of $500 million to $1 billion per year of capital into his preferred niches in Asia.