By Tim Sterk, Investment Strategist – Aegon Asset Management

Active asset managers can use different strategies for adding value to investment funds. One approach is by observing that financial markets have numerous intrinsic characteristics that can be explained by either behavioural finance or by fundamentally driven market skewness, where fundamentals push market prices from their intrinsic value. Fund managers can use those qualities for harvesting what is known as alternative risk premia.

This is the first article in our series on “Alternative Risk Premia”. Alternative Risk Premia provide an uncorrelated source of return that can be added to investment portfolios.

Systematic risk factors: Traditional Risk Premia

Modern portfolio theory as developed by Nobel Prize winner Harry Markowitz, explains that not all investment risks provide higher expected returns. Only the systematic risk factors will give an investor extra compensation, whereas idiosyncratic (or specific) risk factors do not.

Idiosyncratic risk factors are specific for one particular investment, such as regulatory farming changes for an agriculture stock. Systematic risk factors, however, impact all the investments within a certain asset class. An example is interest rate risk for sovereign bonds: moving interest rates impact all bonds. By allocating to (the market beta of) an asset class, you can capture the extra compensation driven by the systematic risk factors.

Since the idiosyncratic risk factors effectively disappear if an investor holds a well-diversified portfolio, Markowitz argued they do not lead to systematic extra reward in the form of additional expected returns.

In accordance with modern portfolio theory, the traditional way of constructing an investment portfolio is via allocation to asset class market betas to access the different systematic risk factors. The compensation that an investor requires in order to expose himself to systematic risk factors, is called traditional risk premia. A risk premium is the extra return that an investor is expected to make over a risk-free investment, such as the safe haven German sovereign bonds. Traditional risk premia can be harvested via asset class specific investment strategies; for instance, via a passive global equity or global bond ETF.

Non-traditional systematic risk factors: Alternative Risk Premia

Next to the traditional risk premia, an investor can increase returns via non-asset class market beta driven risk premia. These alternative risk premia provide an investor with an additional source of return by observing that financial markets possess certain systematic and intrinsic qualities that have a clear and well-understood economic rationale. Those qualities can be used for extracting returns in a systematic manner. These alternative risk premia usually find their origin in either fundamentally driven market skewness or in behavioral finance observations. The concept of alternative risk premia is closely related to the factor investing approach. Though, factor investing is generally dedicated to long-only risk factors, like tilting the portfolio towards the equity value or equity size factor. Alternative risk premia can be captured separately, mostly via the derivatives markets, across equities, rates, credit, currencies or commodities and generally corresponds to long-short portfolios.

Active management of idiosyncratic risks: Alpha

Markowitz argued that no systematic extra reward in the form of additional expected returns is linked to idiosyncratic risk factors. To capture the non-systematic return differences between single securities you need to apply active management. Return differences can be harvested through active deviation from the benchmark investment weights. This source of excess return is referred to as alpha.

As a stylized example we evaluate a bond benchmark that contains 50% German bonds and 50% Italian bonds. Now suppose the fund manager decides to overweigh his German investments by 10% (to 60%) and consequently underweigh his Italian bonds by 10% (to 40%). When the German bonds in the end return 2% and the Italian bonds return 1%, the benchmark will return 1.50%, whereas the actively managed fund will return 1.60%. This means 0.10% of extra value has been added by the active decision to deviate the investments from the benchmark, hence a positive alpha has been obtained.

Expanding the portfolio return drivers?

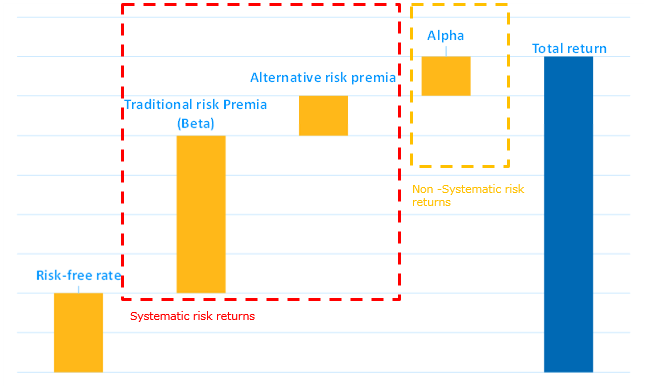

A traditional portfolio construction process is centered on the asset allocation decision and complemented with some asset class specific alpha drivers. Many investors could enhance returns by adding alternative risk premia to their investment mix, thereby increasing the number of return drivers in the portfolio. The graph below shows all these different return drivers in a portfolio. In the coming period we will dive deeper into the concepts of alternative risk premia.

Figure 1: The potential return sources for an investment fund.