By Siddhartha Singh, Managing Director, PineBridge Investments

With Asian markets remarkably resilient to short-term disruptions, the region’s long-term growth catalysts are coming into focus. How can investors maximize these post-pandemic opportunities?

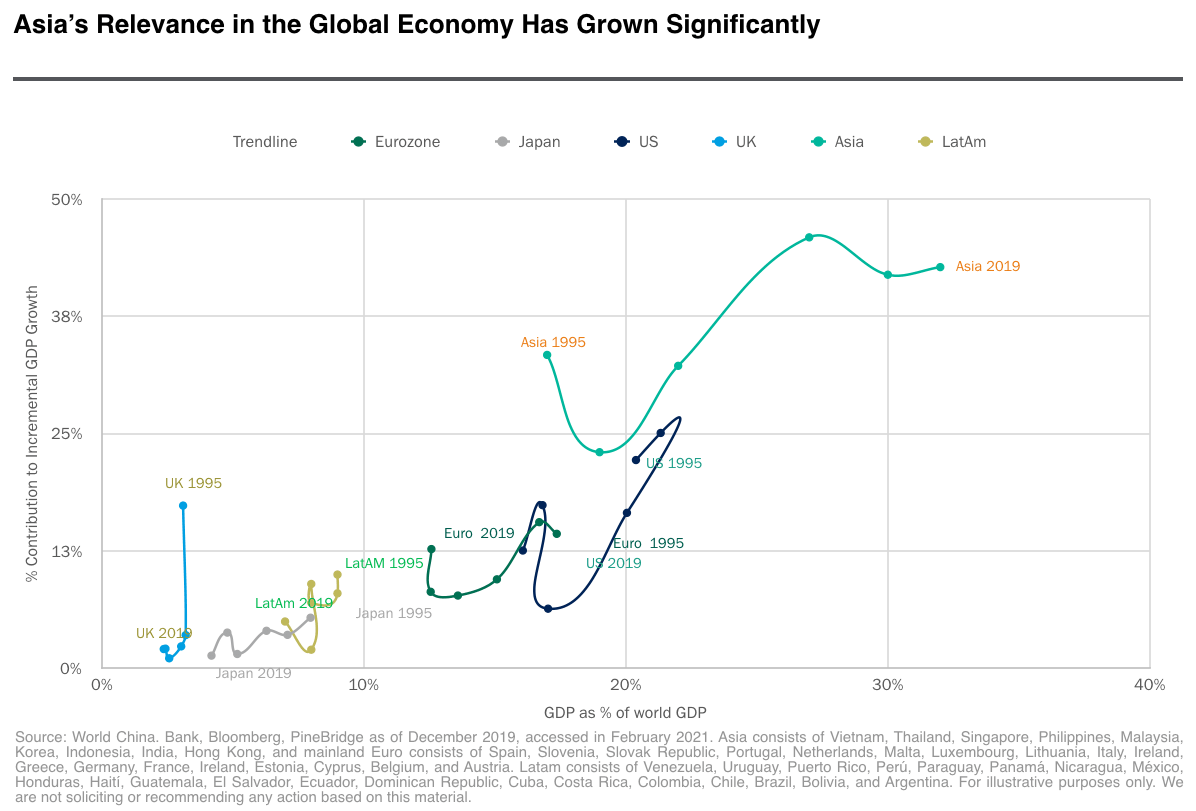

Transformational trends converging in Asia — some accelerated by the pandemic — could potentially unleash the region’s next wave of growth opportunities. In the last quarter of a century, Asia’s phenomenal growth has reshaped the global economy and shifted the world’s economic center to the East.

“Opportunities are where people are. If we take a compass and draw a large circle on the map with Indonesia at the center, and China and India also within it, we will find that there are more people living inside than outside the circle,” says Caroline Loke, Portfolio Manager, Asia ex Japan Equity at PineBridge Investments.

Drivers of post-Covid growth in Asia

With over half of the world’s population living in Asia Pacific,1 then ample opportunities can be found in this region. Urbanization is swelling the region’s cities. Asia projected to have the largest urban population on the planet by 2050 — with implications on essential services, housing, sustainability, among others, for years to come.2

Not only that, the region’s demographics are primed for the next generation of technological innovations incubating in Asia — it has the world’s largest population of “digital natives.”3 This young and tech savvy population is coming of age amid increasing wealth and consumption power. By 2027, 1.2 billion Chinese will join the middle class4 – representing a quarter of the world’s total middle-class population. Such scale has implications on spending from electric cars to education, housing to healthcare, food to finance, and more. And in about 20 years, Asia is forecast to generate half of global GDP and 40% of global consumption.5 Growing demand from Asia could mean a deepening of intra-regional trade and the rise of Asian brands.

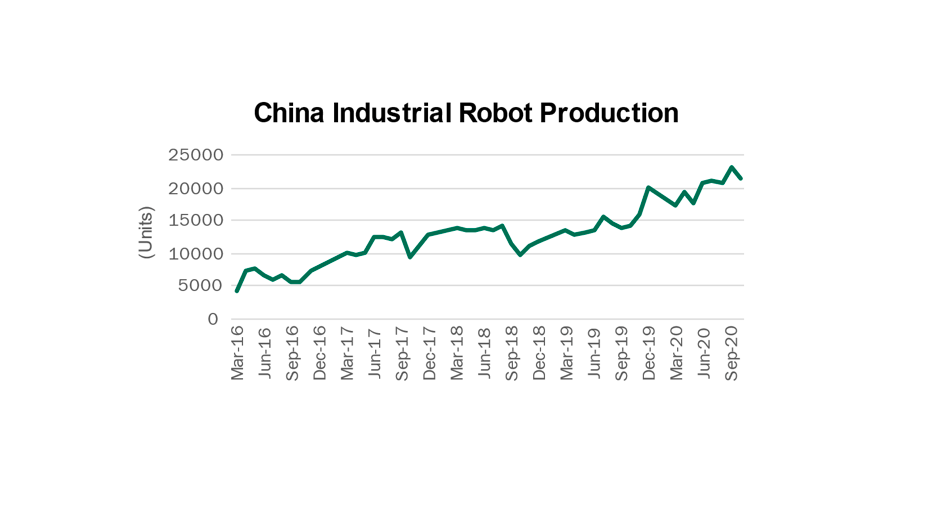

Asia’s growing tech muscle in areas such as automation and robotics, artificial intelligence, big data, and 5G is built upon a strong foundation of research and development (R&D) over the last decade. The drive for self-sufficiency in tech has given rise to domestic industries that aim to rival global peers. China is now the world’s largest market for industrial robots and domestic automation and robotics companies are gaining ground, helping ease labor pressures.6

Source : International Federation of Robotics (IFR), as of December 2020

At the same time, environmental, social, and governance (ESG) issues have increasingly moved to the top of corporate and governmental agenda, with China and South Korea leading the way in net zero carbon emissions goals. Regulatory changes to encourage a greener energy mix, for example, are set to usher in changes to business models — potentially giving rise to new global industry leaders. Loke notes that in the electric vehicle segment, China is now the largest market and the leading EV makers are in Asia, making this industry truly globally competitive.

Uncovering Asia’s future winners

The evolving landscape of post-pandemic opportunities in Asia is shaping up to be markedly different from previous waves of growth, which were manufacturing-led, and are likely to be accompanied by volatility and disruptions, too. For PineBridge Investments’ portfolio managers, active investing — with the flexibility to position across the full universe — is more relevant than ever in uncovering future winners and mitigating risks.

Equities

Asia equities offer a rich ground for finding potential alpha opportunities from these structural changes, with diverse sectors and a growing number of listed companies. In 2020, new listings in Asia picked up, defying the pandemic-induced economic slowdown. Last year, for example, Hong Kong IPOs raised the largest amount since 2010 with over 60% of the funds raised by “new economy” companies such as biotech enterprises.7

As opportunities come from all sectors and company sizes and types, having the flexibility to look for the most compelling companies across the full investable universe is key.

Loke says a benchmark-agnostic approach can help capture mispricing opportunities across the breadth and depth of the market, ensuring broad-based and stable sources of potential alpha through market cycles.

“Free from the constraints of index weightings, this approach, which is at the core of our Asian ex Japan all caps equity strategy, offers the flexibility to adjust capital allocations amid changing company, industry or macro dynamics — making it a potentially better fit for Asia’s constantly evolving markets,” says Loke.

For investors seeking a market-specific exposure, India encapsulates some of these long-term trends – with growing urban populations, accelerating digitalization, and a shift toward green energy. India equities offer access to world-leading companies in information technology services, pharmaceuticals, and chemicals, as well as strong domestic consumption companies.

Elizabeth Soon, CFA, Head of Asia ex Japan Equities and India Equity portfolio manager at PineBridge, says staying above the market noise and focusing on company fundamentals are essential to successful investing.

“We carefully select companies that can see opportunities in the shifting landscape and navigate their way through the transformation,’ says Soon.

On-the-ground research, including company visits and management meetings, is key to assessing the risks and returns of each potential investment, and anticipating and responding timely to market shifts.

Fixed income

In the credit markets, differentiation has become even more important amid dispersion of returns. Asian bonds offer attractive yields to global investors, but investing based on yield alone would miss the nuances at the issuer level.

“Asia is amid an uneven recovery from Covid-19 and transformative structural trends, which suggest significant returns dispersion across the credit spectrum going forward. Selectivity and flexibility in managing your Asian bond exposures across duration, ratings, and yield will be key to portfolio returns,” says Arthur Lau, CFA, Head of Asia ex Japan Fixed Income.

Asia investment grade (IG), for example, is a diverse market in terms of issuer types (from sovereigns to supranationals to corporates), markets, and sectors with a dynamic underlying environment, which lend itself well to active investing.

Across IG and high yield, the team leverages locally based research resources and global sectoral reach to examine credit from both the top down and bottom up.

“This deep sector knowledge is combined with on-the-ground insights to help us create a complete credit picture of the potential returns as well as risks. Having the agility to reposition our portfolio according to market conditions is also important, which may be harder to achieve through index tracking,” says Lau.

Asia equities and fixed income are still largely underrepresented in global indexes despite efforts to increase the weightings of the region’s larger economies in recent years. Given the scale of structural trends underway, investors may not want to miss out on these multi-year opportunities. Stand-alone, high-conviction portfolios offer an alternative to help investors position for and maximize the region’s full potential in the post-Covid era.

Learn more about PineBridge’s Asia strategies, please visit High Conviction Investing in Asia

Notes:

1 UN Population Fund, accessed 10 August 2021

2 See “The Future of Asian and Pacific Cities,” United Nations Economic and Social Commission for Asia Pacific, 2019. https://www.unescap.org/sites/default/d8files/knowledge-products/Future%20of%20AP%20Cities%20Report%202019.pdf

3 Digital natives are generally defined as persons born after 1980. PineBridge estimated the figure based on UN Population data for 2020. There are 3.5 billion people in Asia aged 49 years and under, more than any other region in the world.

4 See “China’s Influence on the World’s Middle Class,” Brookings Institution, October 2020, https://www.brookings.edu/wp-content/uploads/2020/10/FP_20201012_china_middle_class_kharas_dooley.pdf

5 See “Asia’s Future is Now,” McKinsey, 14 July 2019, https://www.mckinsey.com/featured-insights/asia-pacific/asias-future-is-now

6 International Federation of Robotics as of September 2020

7 HKExchange, as of 31 December 2020.

Disclaimer

Investing involves risk, including possible loss of principal. For professional investor use only, not intended for retail distribution. The information presented herein is for illustrative purposes only and should not be considered reflective of any particular security, strategy, or investment product. It represents a general assessment of the markets at a specific time and is not a guarantee of future performance results or market movement. This material does not constitute investment, financial, legal, tax, or other advice; investment research or a product of any research department; an offer to sell, or the solicitation of an offer to purchase any security or interest in a fund; or a recommendation for any investment product or strategy. PineBridge Investments is not soliciting or recommending any action based on information in this document. Any opinions, projections, or forward-looking statements expressed herein are solely those of the author, may differ from the views or opinions expressed by other areas of PineBridge Investments, and are only for general informational purposes as of the date indicated. Views may be based on third-party data that has not been independently verified. PineBridge Investments does not approve of or endorse any re-publication or sharing of this material. You are solely responsible for deciding whether any investment product or strategy is appropriate for you based upon your investment goals, financial situation and tolerance for ris