By Wendy Cromwell, CFA – Director, Sustainable Investment and Portfolio Manager, Wellington Management

Active managers love market inefficiencies. When market participants lack, discount or ignore relevant data, assets become mispriced, and that creates opportunities for active managers to outperform the market. We believe that sustainable investing—which includes environmental, social, and governance (ESG) strategies and thematic and impact investing—is a particularly inefficient market segment.

Here, we discuss five key inefficiencies in this area and how investors may be able to take advantage of them.

1. The market’s focus on short-term growth

Over the past 40 years, the average holding period for equities has fallen from three years to less than one. Increasingly, investors are focused on short-term metrics, such as the next quarter’s earnings per share. Many take little interest in activities such as proxy voting or company engagement, because they won’t hold the stock long enough to benefit from any resulting improvement.

Sustainable investors can extend their investment horizons and engage with companies on material ESG issues in ways that may potentially unlock value over time. We believe that these are strategic business issues that can affect performance. By engaging with companies to understand and advise them, active managers may be able to help them sustain returns and lower their capital costs – which, in turn, should help managers to generate potentially strong long-term returns.

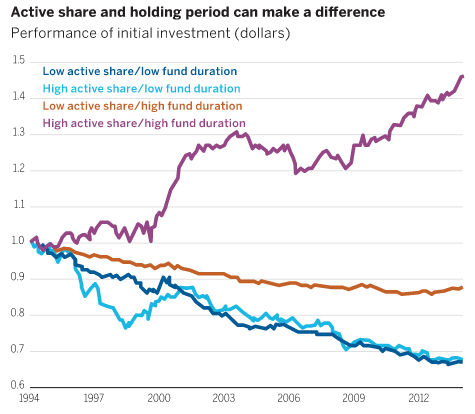

Figure 1 shows the results of one study of funds’ performance based on their active share (how far they differ from the benchmark) and their average investment holding period (here called duration). It found that funds with high active share and long duration significantly outperformed those with either lower active share or shorter duration.

Figure 1

2. Inconsistent, backward-looking ESG ratings

The number of firms that provide third-party ESG scores and ratings is large and growing. While these firms perform a valuable service, their scores are based on company disclosures, which are necessarily backward looking. In addition, each provider has its own emphasis and ways of interpreting data, causing inconsistency in the scoring. While some market participants may believe this is a reason to discount ESG data, we see it as an inefficiency to be exploited.

Researching and engaging with company managements can help active managers reach differentiated, forward-looking insights and more accurately assess the future value of a security. Often, this will mean looking for companies that are improving, rather than those that have already adopted best practices.

We also think active managers can guide companies to better long-term outcomes and financial performance by helping improve ESG practices – for example, encouraging board diversity and independence or advocating better health and safety practices.

3. Emerging market equity indices’ underexposure to structural development

In recent years, emerging markets (EM) governments have changed their policy priorities to support economic development, rather than “growth at all costs.” This is promoting greater inclusiveness, enhanced productivity, improved living standards and better sustainability, which should lead to more stable growth. The key beneficiaries are sectors such as health care, consumer products and technology. However, EM indices are still largely weighted towards past drivers of growth, such as natural resources and financials. To us, this suggests that investors who hug the benchmarks are underexposed to development-related sectors, which have the potential to outperform over the coming decades.

We believe it is possible to take a differentiated, longer-term approach to EM equity investing, by focusing on development, rather than cyclical growth. The result would be a portfolio weighted towards the sectors and companies that are likely to benefit most from policymakers’ drive to make economic progress more stable and inclusive.

4. Blind spots in climate risk analysis

Climate change poses two types of financial risks: transitional risks from changes in climate-related policy, regulation and legislation; and the physical risks from drought, flooding, rising sea levels and so on. In our view, most climate risk analysis currently focuses more on the transition risks. To us, this is a massive information blind spot, as we believe that the physical risks of climate change will have profound impacts on asset prices around the world.

We believe it is possible to exploit this inefficiency by bridging the gap between science and finance. Wellington has been working with Woods Hole Research Center, a leading independent climate research institute, to understand the implications of six climate factors (heat, drought, wildfire, hurricanes, floods and water availability) for securities, industries and economies. For each factor, we seek to identify the most relevant metric and draw maps showing how different regions are projected to be impacted over time. We then use these maps to assess which securities are likely to be most affected and whether this risk is priced in.

5. An undefined impact investing universe

Industry groups have made great progress on impact measurement and reporting standards, and the United Nations Sustainable Development Goals offer an important framework. But impact investors still have to establish their own impact criteria and research for themselves which companies qualify, and this takes resource and effort.

We have identified a universe of nearly 500 publicly traded equities and a fixed income universe of approximately US$1 trillion that goes beyond bonds that are labelled green or impact. We believe it is critical to analyse impact companies/issuers with a non-traditional lens. For example, a company that converts solid waste into energy may be compared with a traditional waste-management business model. But that can lead to mispricing, as the fortunes of waste-to-energy companies depend more on the prices of recycled metals and energy than on traditional inputs.

Conclusion

We believe that the inefficiencies in the sustainable investing segment give active investors, drawing on thorough analysis and proprietary research, ample opportunities to generate outperformance over the long term.

*Source for “Figure 1” above is “Patient Capital Outperformance: The Investment Skill of High Active Share Managers Who Trade infrequently” by Martijn Cremers (Notre Dame), Ankur Pareek (Rutgers Business School), December 2015. More recent data from this source is unavailable. Although we believe that the research and findings are still valid, updated data could provide different results.