By Aviva Investors Fixed Income Team

Halloween is synonymous with zombie movies. In almost every film, the scenario is the same: a clutch of survivors resists as the living dead contaminate ever more people around them.

Never has this appeared so apt as in 2020. Dramatic falls in revenues are pushing many companies to the brink but, propped up by unprecedented central bank support, they have so far managed to survive. These are the zombie firms which, by the definition used by bond investors, are issuers generating profits lower than the interest payable on their debt for at least three years. To stay in business, these firms must borrow more just to pay the interest they owe.

Elixir of life

Almost every sector of the economy has been disrupted by COVID-19, particularly consumer-driven services. In the latter, we have seen huge levels of issuance as companies scrambled to shore up cash for the months ahead. This has been possible thanks to the generosity of central banks pumping liquidity into markets and, in the case of the US Federal Reserve, explicitly supporting high-yield issuers through its bond purchase programme.

The European Central Bank is not buying high-yield bonds directly, but there is a trickle-down effect from its support to investment-grade issuers, and from traditional investment-grade investors searching for higher yield to achieve their income targets. That said, the pickup in fund flows has remained much more muted in Europe than the US (Figure 1).

Rise of the zombies

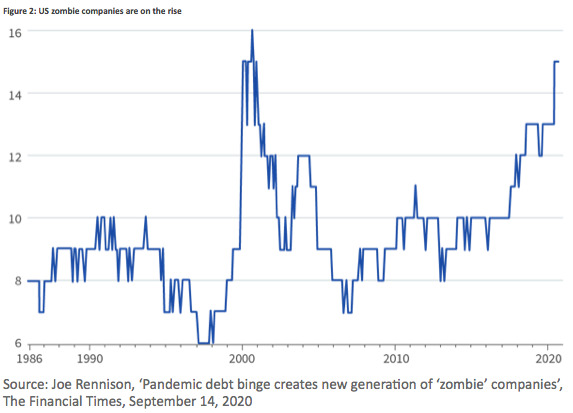

Coupled with massive debt issuance, the absence of decent revenues – or any revenues at all – has created a cohort of zombie companies on both sides of the Atlantic, which have been widely discussed in in the media and in a recent report by the Bank of International Settlements (BIS). Unsurprisingly given the economic backdrop, the number of companies that can be classified as zombies is rising, as Figure 2 shows.

The first worry for investors is that these companies begin to default en masse once their resources are exhausted and they can no longer find new lenders. On this front, the news is reassuring, at least for now.

“Expectations of defaults are decreasing and should stay low as long as monetary policy remains supportive,” says Brent Finck, senior high-yield portfolio manager at Aviva Investors. “In addition to central banks’ bond buying, the liquidity they are injecting in markets needs to be invested somewhere, allowing companies to find takers for their issuance. There is no expectation for this to stop in the near future.”

During the sell-off in March, J.P. Morgan’s Default Monitor was projecting default rates for 2020 at above 10 per cent. This was when concerns over the economic impact of COVID-19 were heightened and prior to the announcement of fiscal and monetary support by governments and central banks.

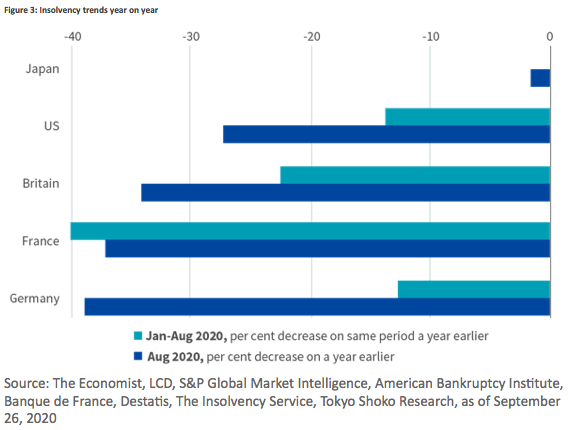

But by the start of October, forecast default rates for US high-yield bonds were down to 6.5 per cent for 2020, and as low as 3.5 per cent for 2021. Although dismal economic growth suggests bankruptcies should rise, so far they are lower than in 2019 (Figure 3).

Zombification or new lease of life?

It could go wrong. Much of the recent news flow underlines the risks of zombie companies surviving indefinitely, keeping capital invested in less productive parts of the economy with a dampening effect on inflation, interest rates, innovation and growth.

However, in a free-market economy, it should always be possible for vibrant, entrepreneurial companies to win business.

“Modern and efficient companies are set up to take advantage of complacency or inefficiency elsewhere, meaning even if zombies survive for longer because of central bank assistance, they should not be able to do so for ever,” says Stewart Robertson, senior economist at Aviva Investors.

In fact, while the BIS report suggested the survival of zombie companies may crowd out investment and employment in healthy firms, this is not evidenced across the board. The authors concluded: “It is important to consider expectations of future profitability in addition to current profitability when classifying firms as zombies.”

For instance, when Japan finally started to tackle weakness in its banking sector in the 2000s, the share of zombie firms fell rapidly, in part because those firms became profitable once again rather than going out of business.

Where COVID-19 makes it more difficult for investors is that low revenues and high leverage can now be found both in companies that were already on their way to zombification before the pandemic, but also in previously healthy firms that now need cash to survive long enough to resume their activity.

“The market needs to realise that having liquidity is helpful, but it won’t create revenues for you, and it won’t create earnings for you. This means managers have to be increasingly diligent when analysing companies’ leverage levels and cashflows. The challenge will be finding sectors that are particularly resilient,” says Josh Lohmeier, head of US investment-grade credit at Aviva Investors.

Cruise lines are a good example. Until the pandemic is brought under control, they are almost entirely unable to sail and have no revenue potential, while burning cash to the tune of several hundred million dollars a month ($650 million a month for CCL, for example).

“The sector has seen one issuance after another as firms raise liquidity on the presumption that, if they can survive until the end of 2021, a vaccine will have resolved the issue by then, allowing them to resume their operations and profit-making,” explains Paul Janowitz, senior credit analyst at Aviva Investors.

The same is true within sectors, where some companies are doing better than others, even though all are easily placing their debt. For example, Las Vegas casino operators are struggling and should have restructured without Federal Reserve support, according to Danielle DiMartino Booth of Quill Intelligence, whereas regional casinos began recovering once lockdowns lifted.

The devil is in the detail

What is less talked about, but more concerning, is the degradation in covenants. With the continued strong demand for high-yield bonds and record issuance from businesses trying to stay afloat, the quality of covenants is deteriorating.

Covenants typically impose restrictions on the amount of leverage permitted on a company’s balance sheet, complemented by an obligation to seek existing bondholders’ approval before issuing additional debt and potential penalties to pay when leverage hits certain ratios.

Across global high-yield markets, the level of demand has given issuers more bargaining power to loosen those restrictions. Some issuers have also found loopholes whereby the amounts used to report their leverage levels do not reflect their actual cashflows. This allows them to add debt without triggering ratios, consent fees or the need to seek approval from existing investors.

At the higher quality end, this year has also seen a large increase in fallen angels. “As investment-grade companies, they typically did not require covenants, and many have continued to issue bonds as high-yield firms without investors requiring them to change their practices,” says Sunita Kara, senior global high yield portfolio manager at Aviva Investors.

This is worrying because covenants are designed to protect existing investors from exposure to unwanted risk, such as when a debtor company issues new bonds. Without these in place to restrict issuance, the quality of bonds may degrade without investors being adequately compensated for the additional risk, or even consulted as to whether they are willing to take it on.

Combined with the difference in fundamentals across sectors and firms, weaker covenants are leaving investors exposed. Understanding companies’ leverage levels, but also their business models and prospects for renewed profitability in the medium term, is more important than ever to avoid falling victim to the continuing march of the zombies.

Aviva Investors regularly post comments and analysis on the credit markets. Click this link to see their latest updates……