By Hamlin Lovell, NordicInvestor

Yields on prime Swedish commercial real estate have touched all time lows, ranging from 3.5% for Stockholm offices to 4% for Gothenberg or Malmo offices, or shopping centres; 4.8% for logistics and 5.25% for retail warehouses, according to Savills Sweden, as of late 2018. Higher yields on property outside the Nordics are partly a function of higher risk-free interest rates, but even after accounting for interest rate differences there is still potential to earn higher income overseas.

The section below reviews presentations made in May 2019 to the Amsterdam chapter of the CAIA (Chartered Alternative Investment Analyst) Association.

Tim Bellman, Head of Global Research for INVESCO Real Estate, has watched Asian property markets evolve during his sixteen years based in Hong Kong between 1991 and 2007, and subsequently as part of his global purview. In 2019, he argues that Asia offers more attractive yields and hence is an overweight position, but this was not always the case. Bellman recalls how in 2009-2010, pricing was strongly in favour of the US.

Over the next few years, he expects Asia Pacific to be the strongest performing property region globally, and judges valuations to be fair relative to bonds. Meanwhile, accommodative monetary policy lessens valuation risk. Bellman has a constructive outlook because the region is forecast by Oxford Economics to grow by 4.5% per annum out to 2021, and will continue to grow its share of the world economy. Asia is expected to make up 55% of the world’s urban population by 2030. Urbanisation is another driver for property demand in some markets. The Asian city states – Hong Kong and Singapore – are already, in effect, 100% urbanized, while Japan and China have reached rates of 80%. India has substantial scope to increase its city-based population.

The listed investment universe is large and growing. Asia Pacific already makes up one third of the market for listed real estate companies, according to Cushman & Wakefield, with 40% coming from China (mainly: Shanghai; Beijing; Shenzen and Guangzhou);20% in Japan and the remainder including Australia, South Korea, Singapore and Hong Kong. New legislation in India has spawned the first local REIT, Blackstone-sponsored Embassy Office Parks REIT, which floated on the Mumbai market in April 2019 and should blaze a trail for the Indian REIT market.

Transparency is improving, too. Australia and New Zealand have for long ranked alongside the UK and US as some of the most transparent markets, and recently tier one companies in China have made great strides in becoming more open; Japanese firms have also raised their game on transparency, and Singapore and Hong Kong also offering reasonable transparency, according to the JLL Global Real Estate Transparency Index. This is based on criteria including governance of listed and unlisted vehicles; regulatory and legal frameworks; transaction processes, and sustainability measures. Liquidity also now compares well with developed Europe and the US, according to the Real Capital Analytics (RCA) Capital Liquidity Score, which considers absolute and relative liquidity measures.

The Dutch experience

Dr. Maarten Jennen, real estate investment strategist at Dutch pension fund service provider PGGM, shared his experience with investing in Asian real estate markets. PGGM, which has over EUR 200 billion in assets under management of which c. EUR 25 billion in real estate, has been investing in Asia-Pacific property since the late 1990s. Its first investments in the APAC region were in Singapore, Hong Kong, Japan and Australia and remains focused on the largest, most transparent and liquid markets in the region. In 2006 PGGM was one of the earlier institutional entrants into the Chinese property market and has been active in that market ever since. At first, PGGM only invested via funds, but over time increasingly also through joint ventures and club deals which provide the benefit of improved control over the investment and lower costs. Jennen realizes that this investment format is only available for the larger investors.

PGGM’s real estate investment team is fully based at its HQ in Zeist, in the Netherlands. Through strong relationship management and establishing long term structural partnerships the team has been able to make successful investments in distant markets where local market knowledge is key.

PGGM now has approximately one third of its private property allocation in the Asia-Pacific region. A weight expected to remain fairly stable as Jennen has confidence in continued long term economic growth and positive impact of the demographics, technology, globalization and urbanization megatrends. PGGM’s global private property allocation has realized a cumulative total return of 112% since the end of 2009, outperforming the 94% growth seen in the global index over this period. Part of the outperformance has come from the Asia Pacific allocation, which is up by 126% thereby outperforming both the overall portfolio and the global index.

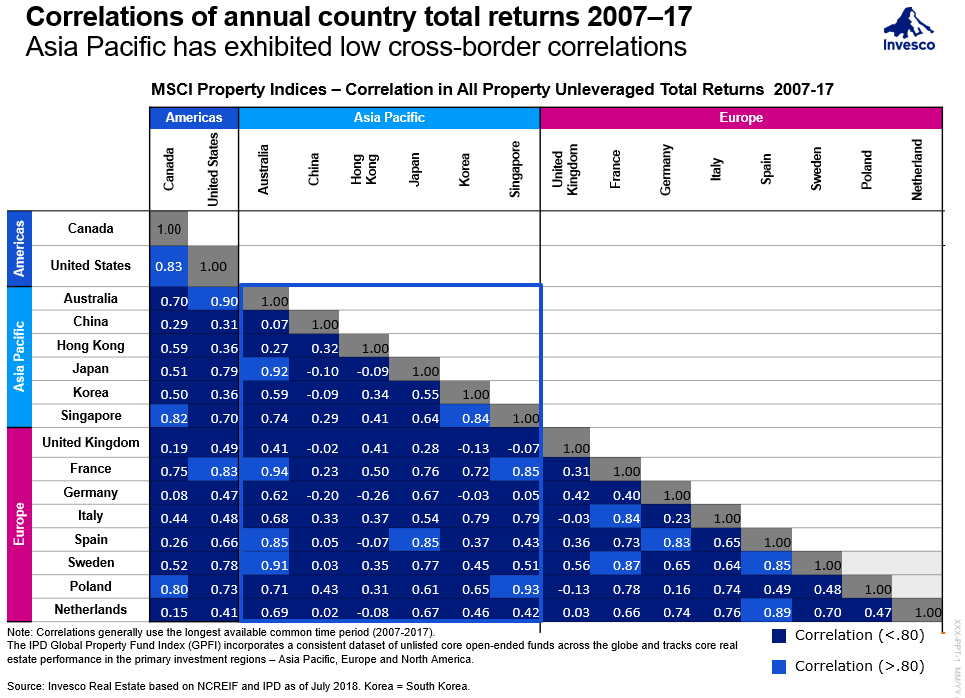

Diversification benefit

The most developed Asian property markets have historically (between 2007 and 2017) offered very limited diversification benefits versus Swedish property: Australia has a 0.91 correlation and Japan a 0.77 correlation.

But some other markets in Asia offer a much bigger diversification benefit: the coefficients are 0.03 for China, 0.35 for Hong Kong, 0.45 for Korea and 0.51 for Singapore. Correlations within Asian property are quite low, so an appropriately diversified portfolio can smooth out returns.

Sub-sectors within Asian property

Asian property is a diverse asset class, where it pays to select geographies and sub-sectors carefully

Bellman pointed out that in 2019, it is important to be selective as rental and NOI growth is slowing, as global economic growth moderates. His preferred segments and geographies include logistics and offices in Australasia; and offices and residential in certain Japanese cities.

It is possible to find assets in segments such as logistics that are more geared to the secular domestic economic growth story rather than to the more cyclical export economy. The structural growth in logistics is driven by the megatrend of growing internet and mobile shopping. Invesco has invested in three logistics projects in Shanghai and one in Siheung, just west of Seoul in South Korea.

Tier two cities in some countries such as Japan may offer superior rental growth to tier one locations: in Fukuoka; Hiroshima; Kyoto; Nagoya; Osaka; Sapporo and Sanchai, rental growth can be much more robust as office vacancy rates trend down. Invesco made an opportunistic investment into a class B property in Osaka, refurbished and re-leased it, and generated an IRR of 20%. And Australia’s tier two cities – Adelaide, Brisbane, Canberra, Perth – can offer a 1.5% to 2% spread over Sydney. To some extent this can be viewed as a premium for greater illiquidity and volatility, but investors with long time horizons should be able to enhance returns.

Australian banks’ more cautious approach to property lending opens up opportunities for non-bank lenders to enter the fray and provide finance at attractive yields. Senior tranche and mezzanine loans with a loan to value ratio around 60% have generated IRRs as high as 18%. Going forward, given the lower interest rate environment and increased participants, the returns in this space are likely to decrease.

Hong Kong is being avoided as valuations are inflated by strong demand from locals, and heightened downside risks due to the trade war between China and the US as well as the domestic social unrest.

Of course, there are unique risks in Asia. Indonesia’s Jakarta will soon be underwater, and the capital city is being relocated. A “wild card” risk is that an escalation of the US/China trade could conceivably lead to confiscation of assets. Currency volatility is another factor to contend with, but Bellman takes the view that this risk should even out over time for long term holders.